MesoLive development update #1

Introduction

It’s been a while since we started working on MesoLive - the Live version of MesoSim. It’s a good time to give an update on what has been achieved so far.

Before we dive into the specifics here are the requirements driving the development:

- MesoLive must become an excellent position, strategy, and account monitor

- It must support the deployment and management of trading strategies developed in MesoSim

- It has to be accurate, secure, and affordable

Based on the above requirements MesoLive is not a replica or clone of any other software. It’s a new way of addressing the real pain points of options trading today.

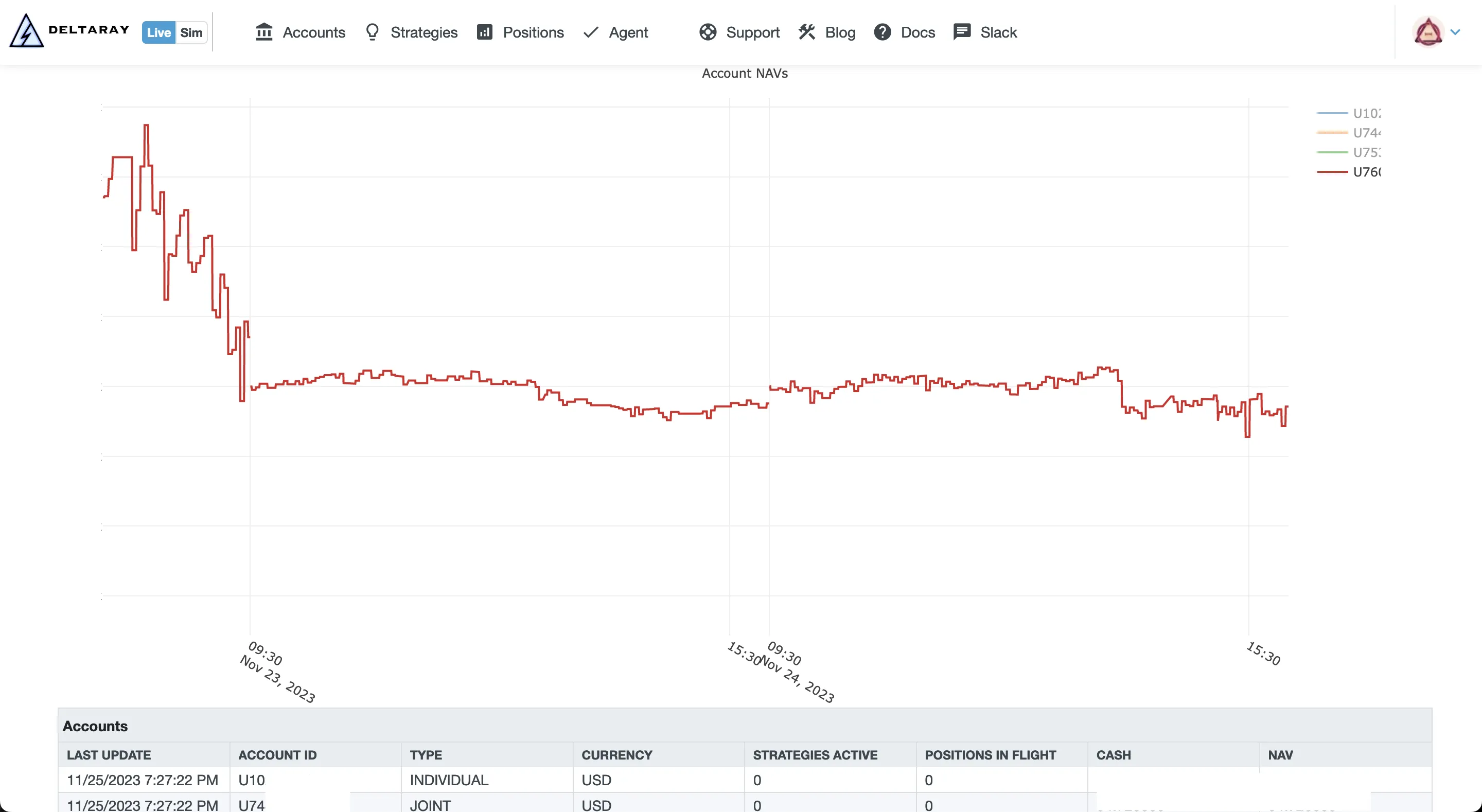

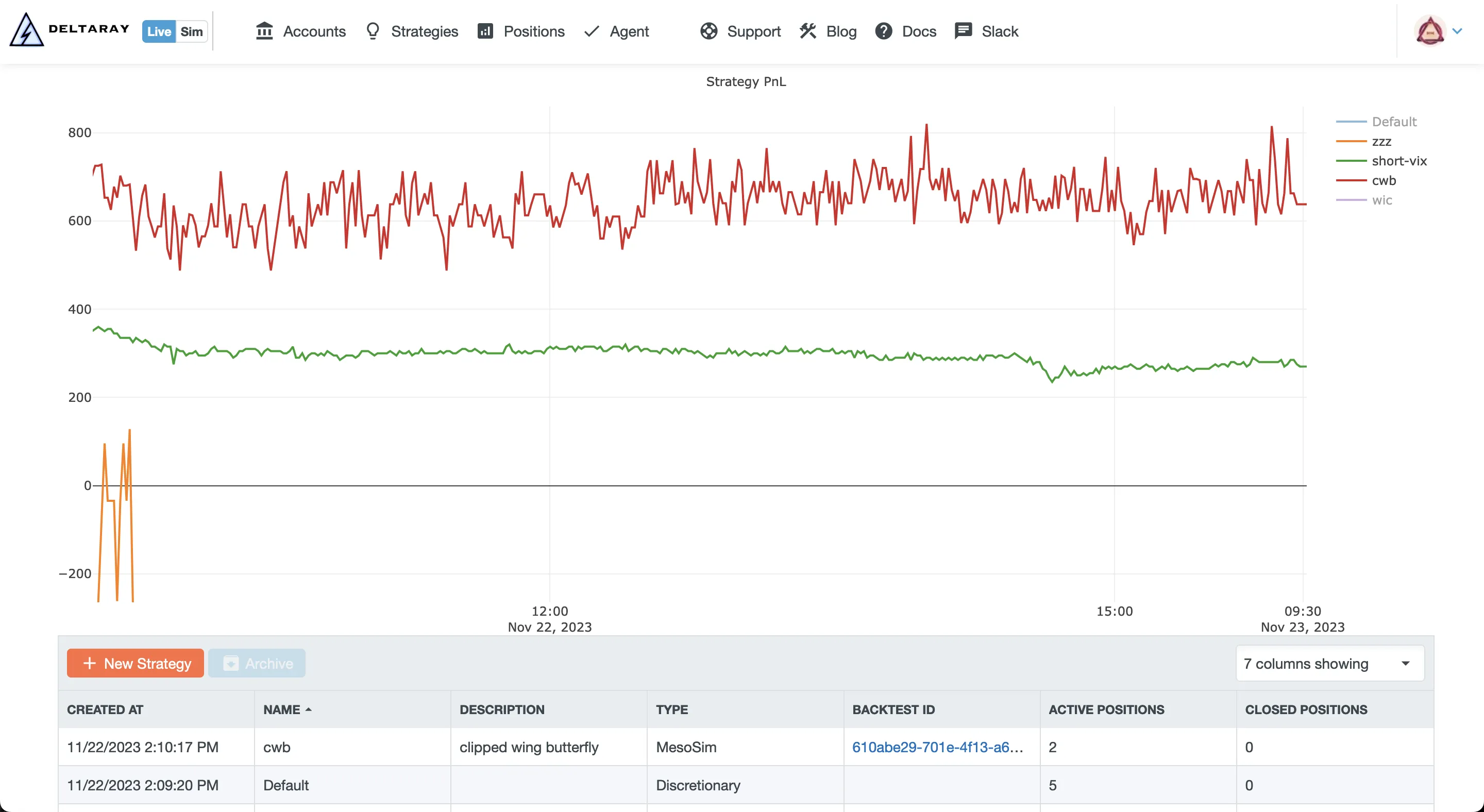

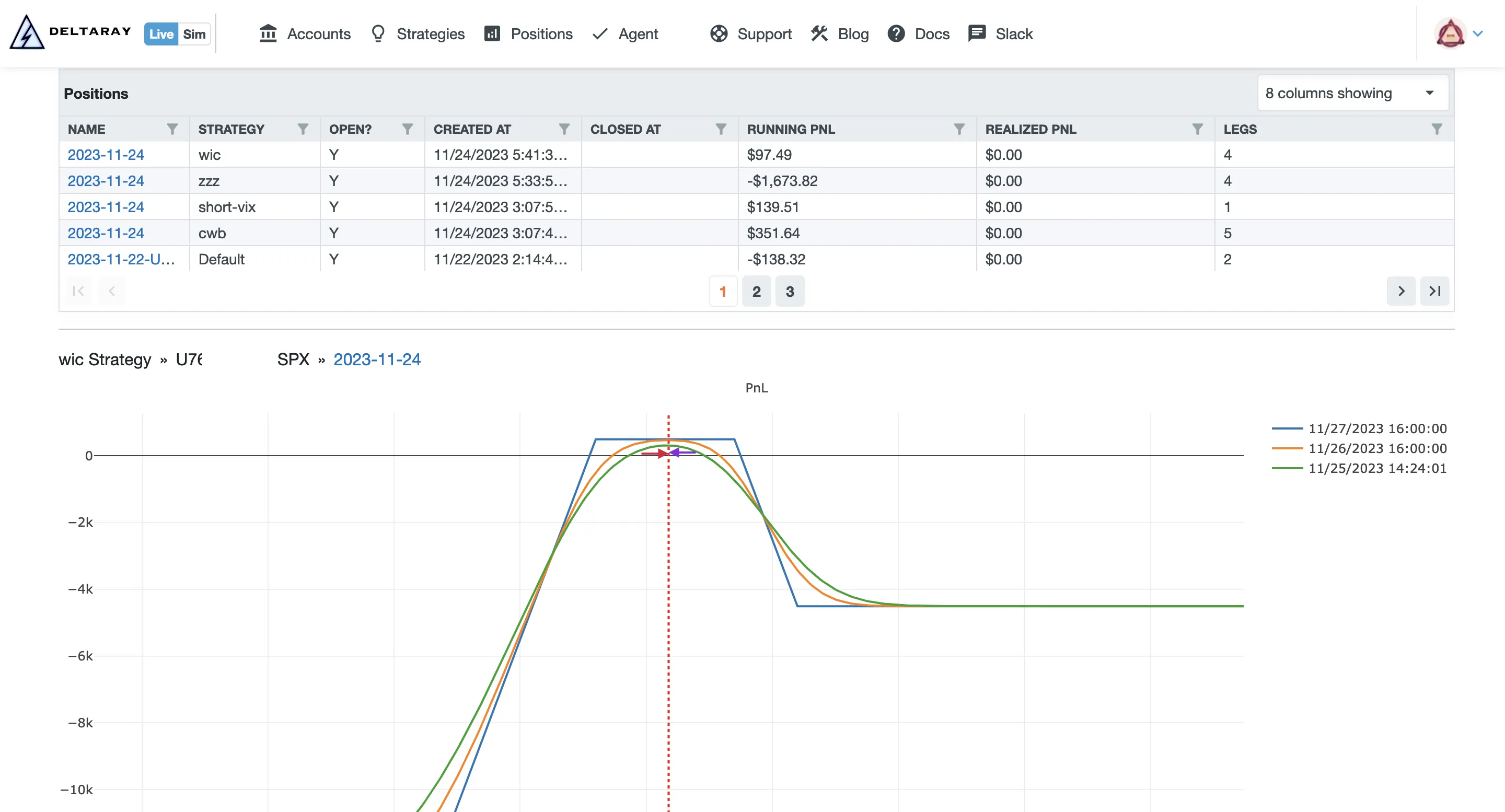

Position / Strategy / Account Monitoring

State of the art

The majority of time spent in trading is dedicated to monitoring open positions and waiting for Profit Target or Stop Loss to be hit. While brokerages offer the tools (TWS by IBKR, ThinkOrSwim, or TastyTrade’s app) which display live positions and certain risk metrics, they lack the following functionalities:

- Organizing Legs into Positions

- Assigning Positions to Strategies

- Tracking Position and Strategy PnL and Greeks over time

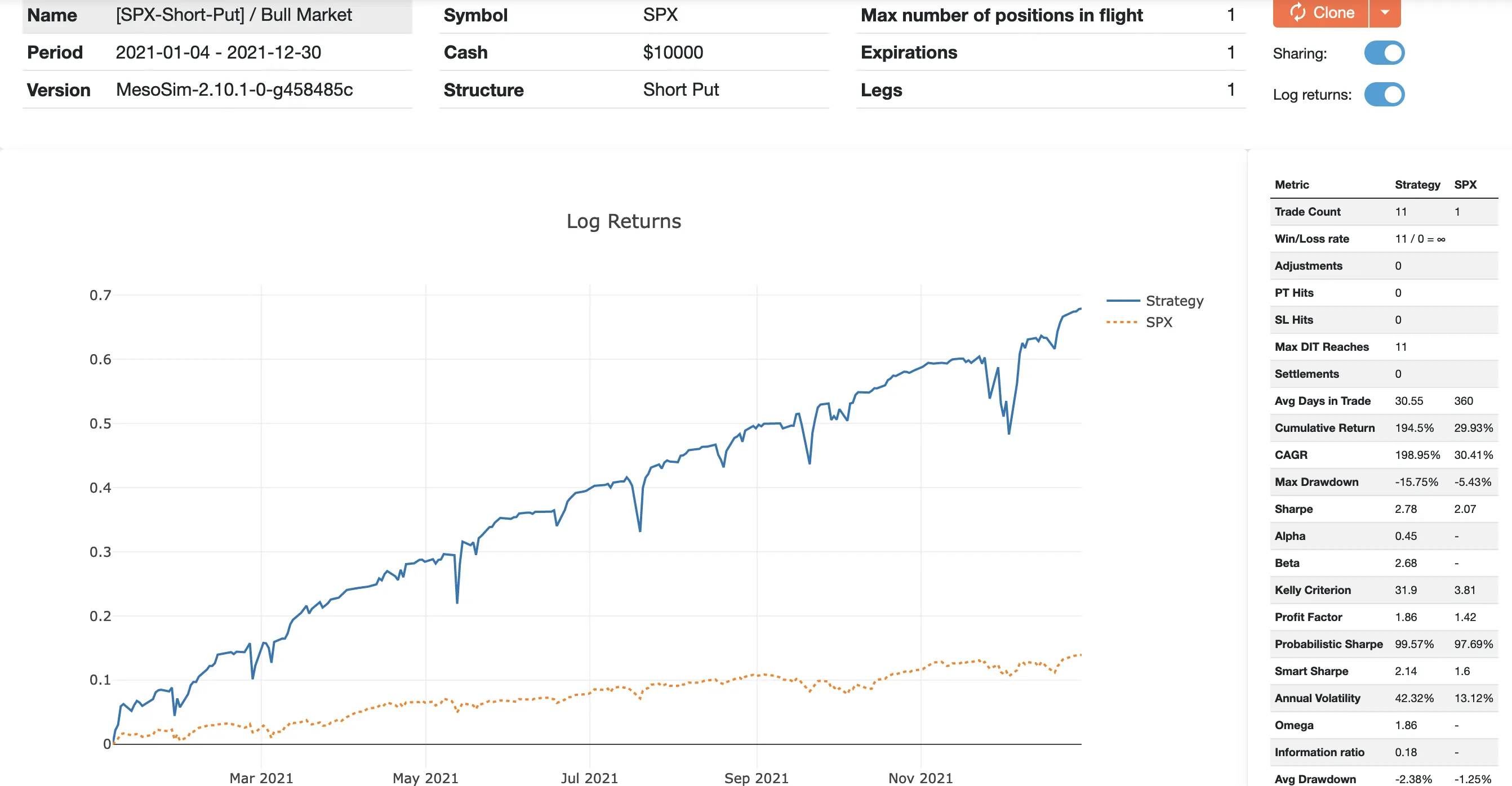

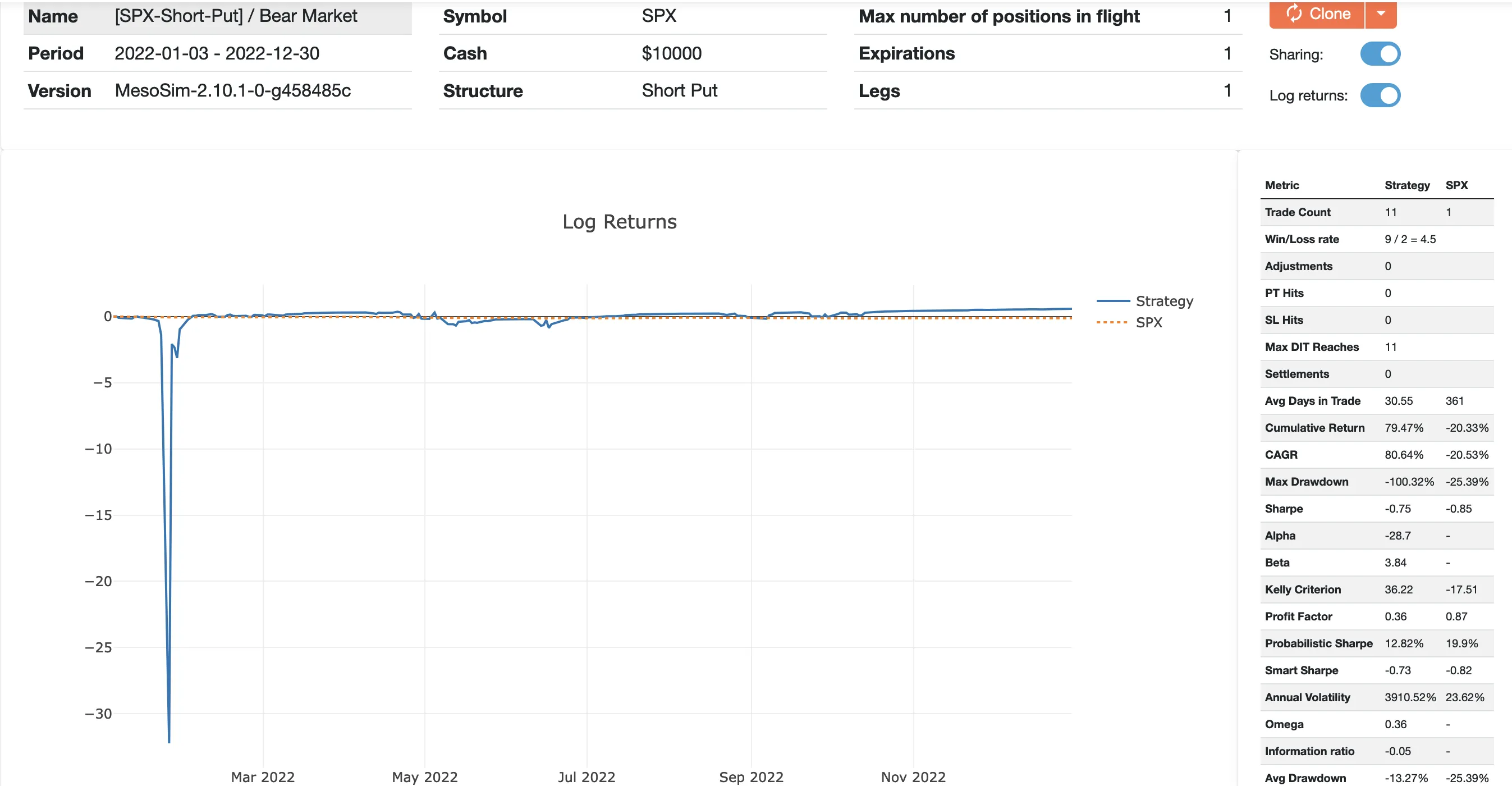

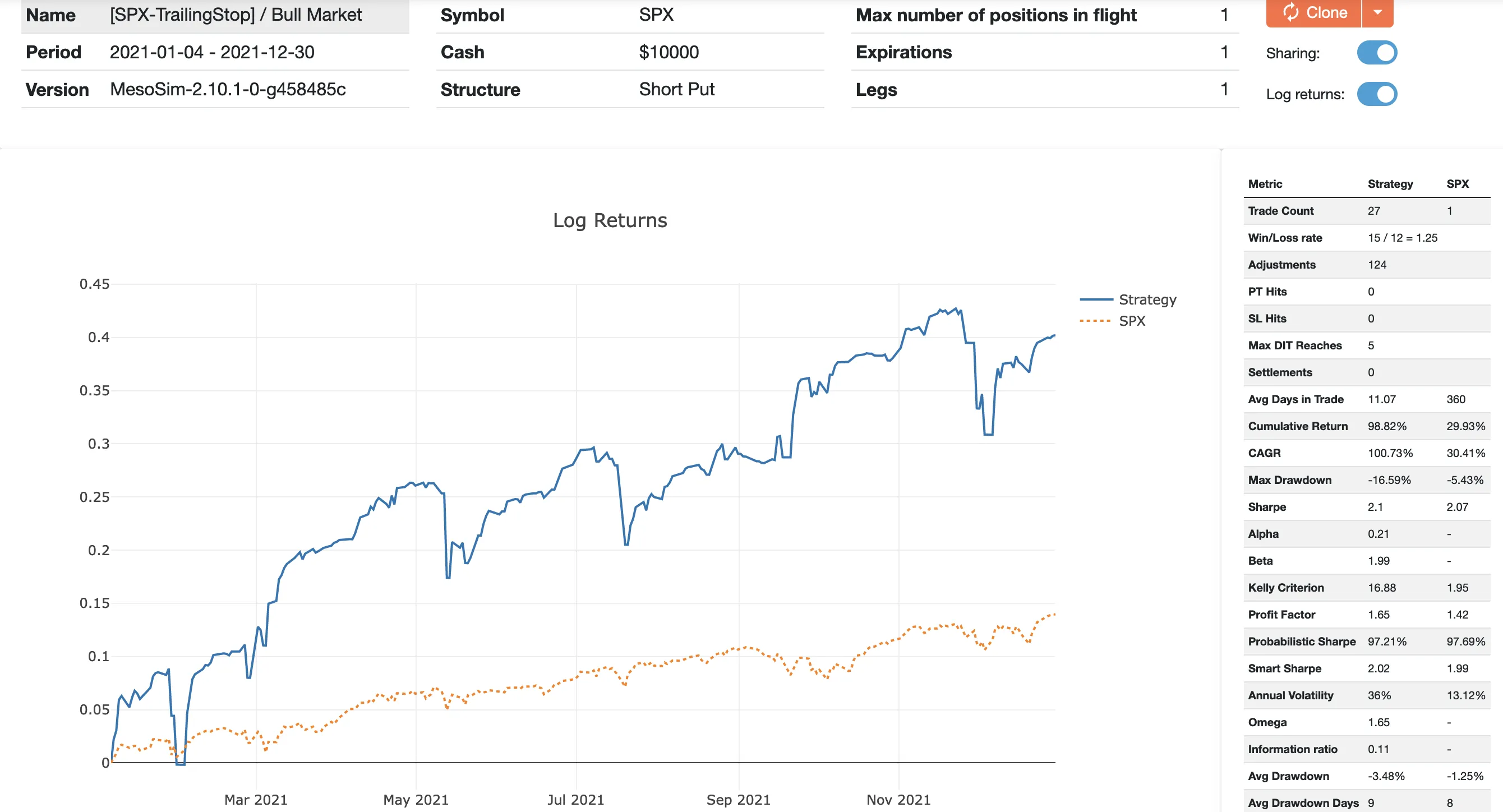

The most frequently used analytical tool for Options Trade by retail users - OptionNet Explorer (ONE) - bridges some of the gaps, but it still falls short on the following points:

-

Moving legs around is cumbersome:

One needs to specify trade details (such as entry price and commission) manually. -

Low-resolution PnL chart on a strategy level:

Just the realized PnL is shown, but intra-trade drawdowns and quantitative metrics are missing. -

Limited information on Greeks:

- Historical charts of greeks over time are absent.

- Greeks are shown only at T+0 and not projected to the future.

Therefore, people (including us) often track their trades not just in ONE, but in a tracker Excel or Google Sheets. This approach works but takes a lot of time to administer.

MesoLive’s approach

With MesoLive we are addressing the above pain points by

- Automatically Tracking Positions, Executions, and Account information, eliminating the need for manual entry of fills

- Combining legs on the fly to make up a positions

- Assigned positions to Strategies

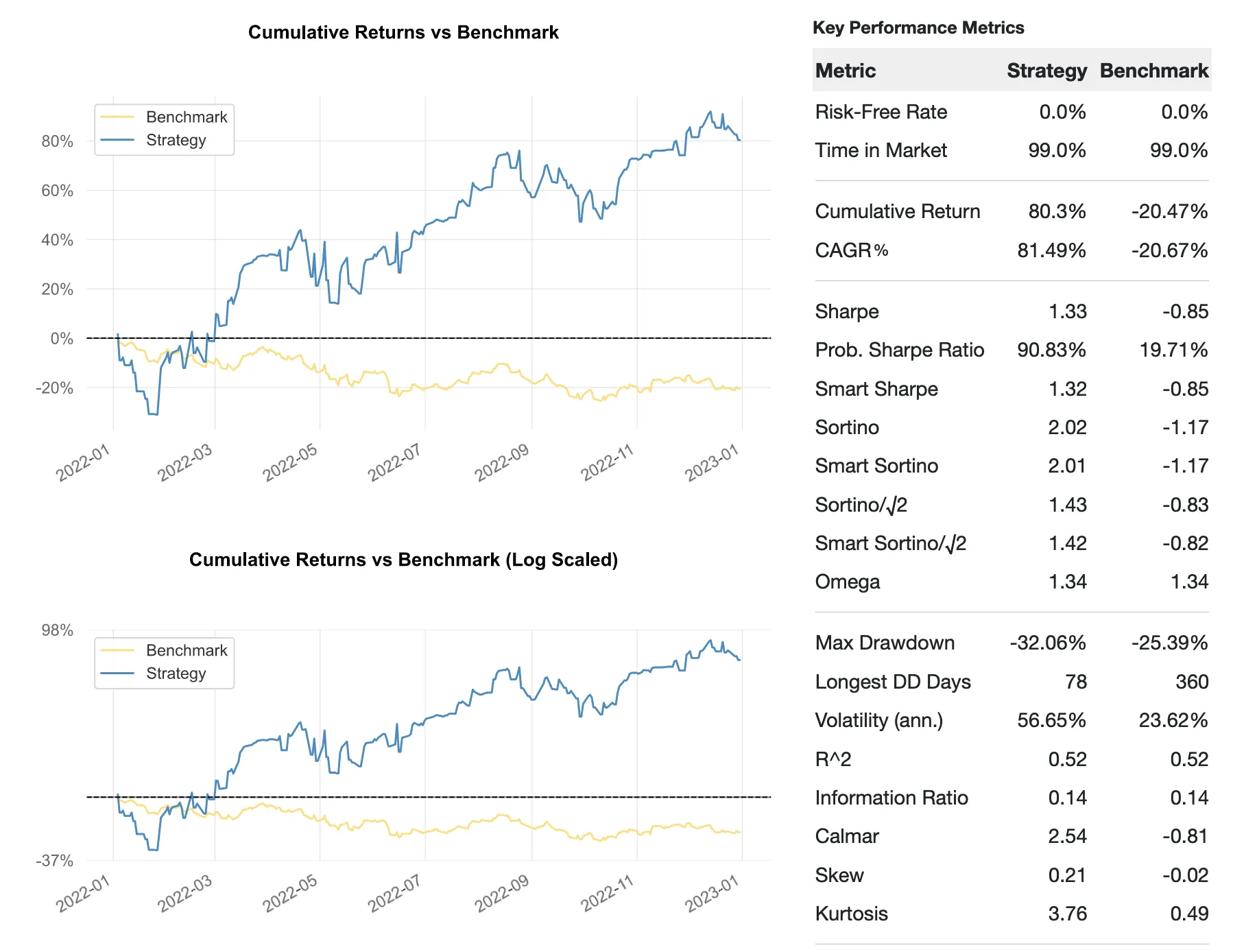

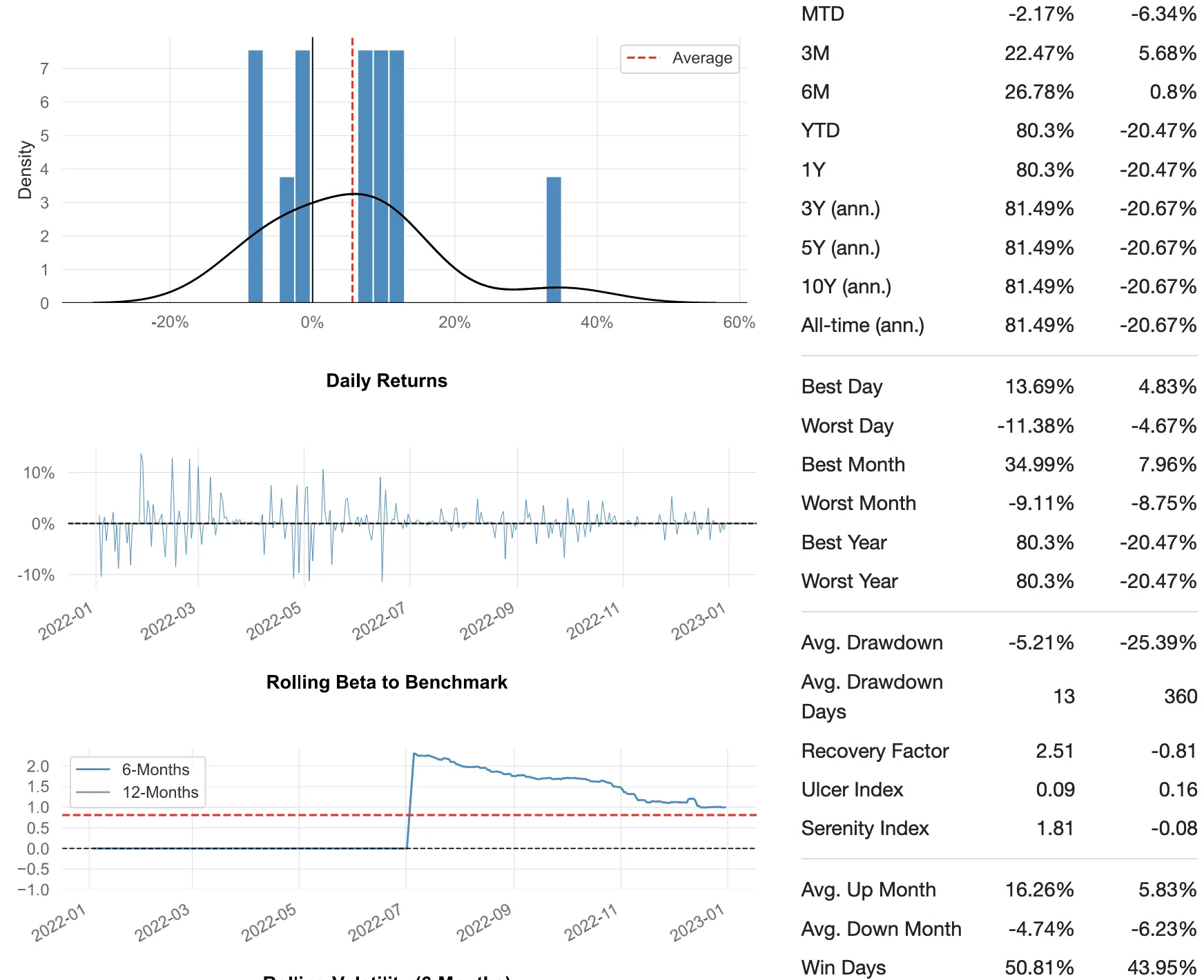

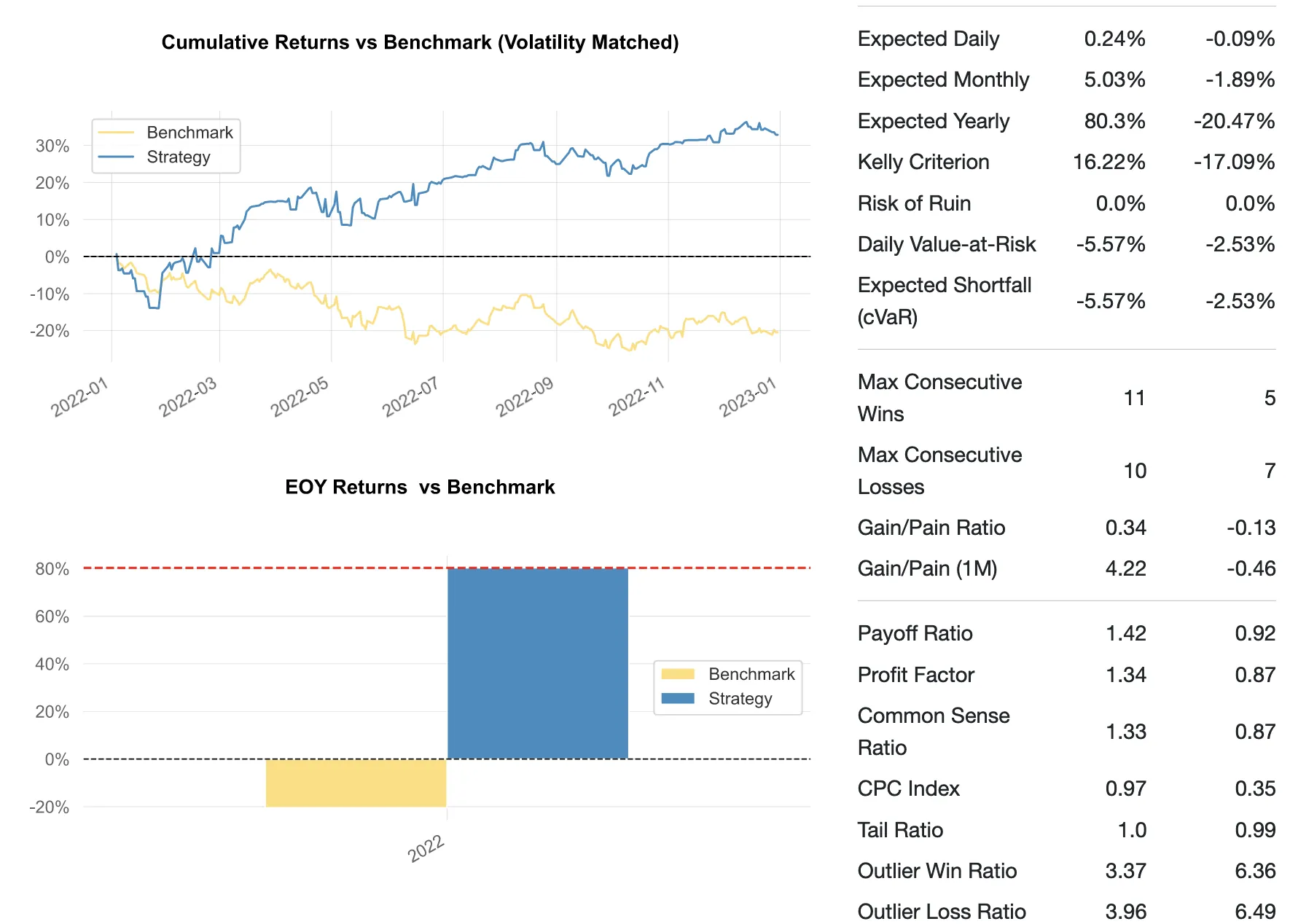

- Collecting Position, Strategy, and Account level PnLs and Greeks frequently (every minute)

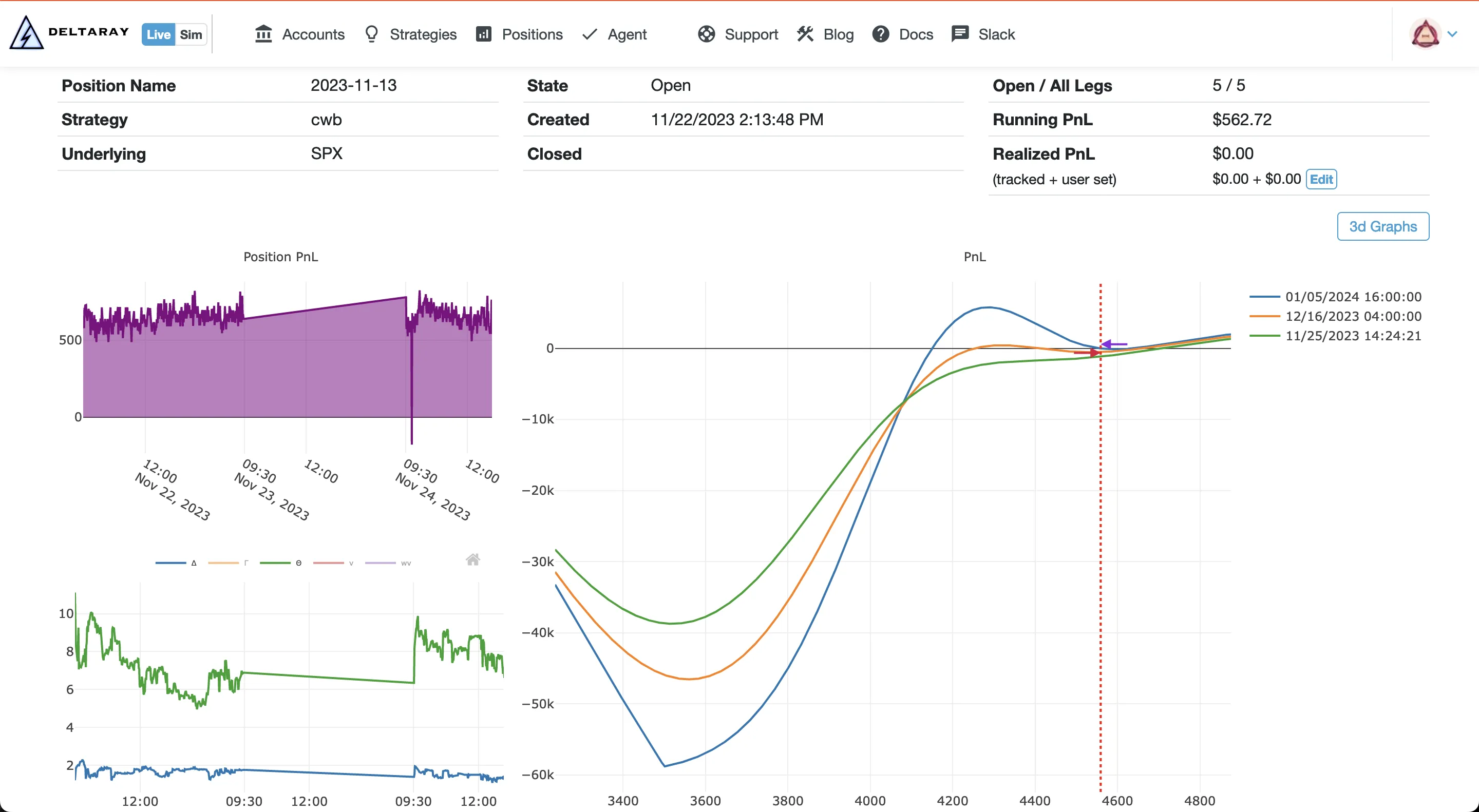

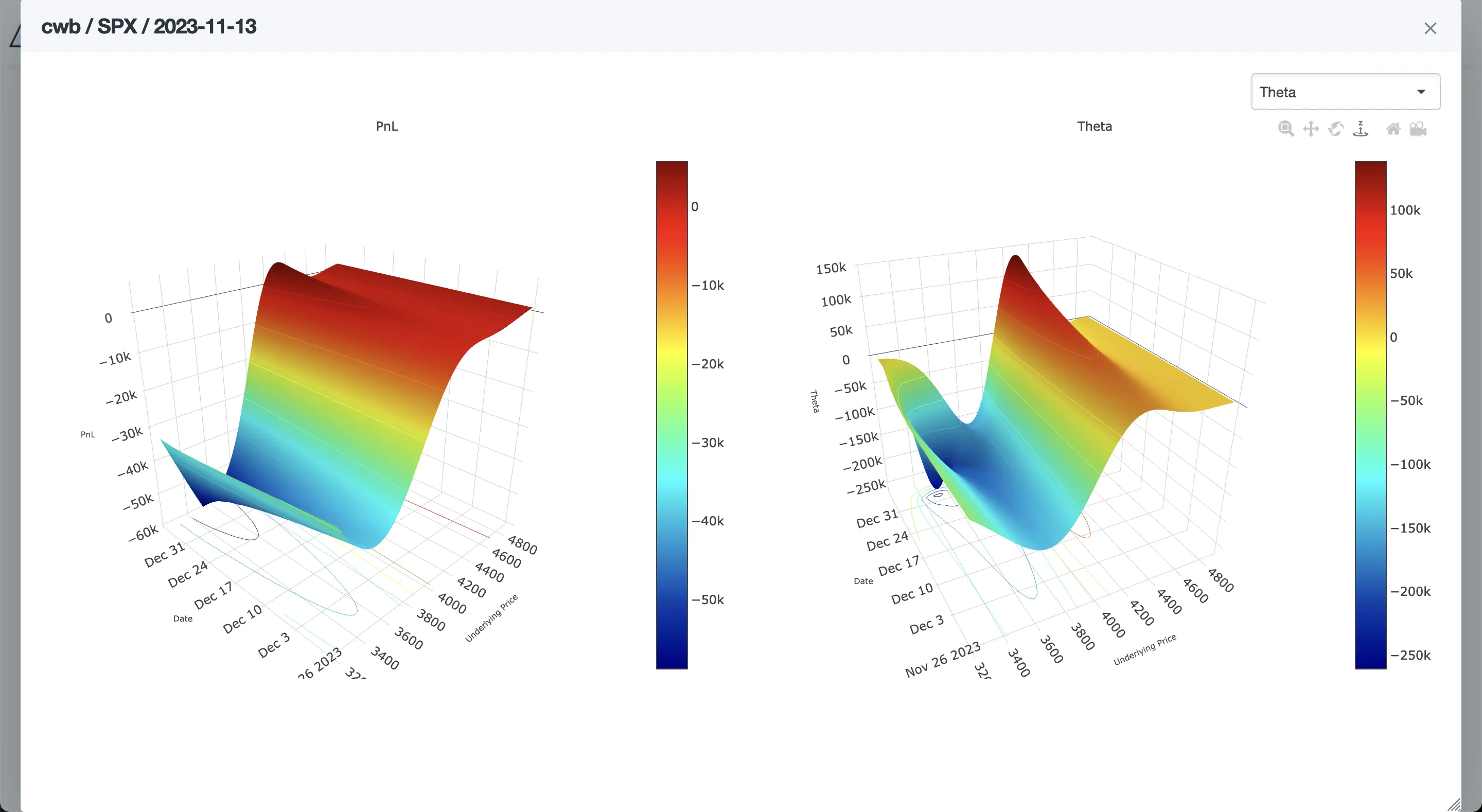

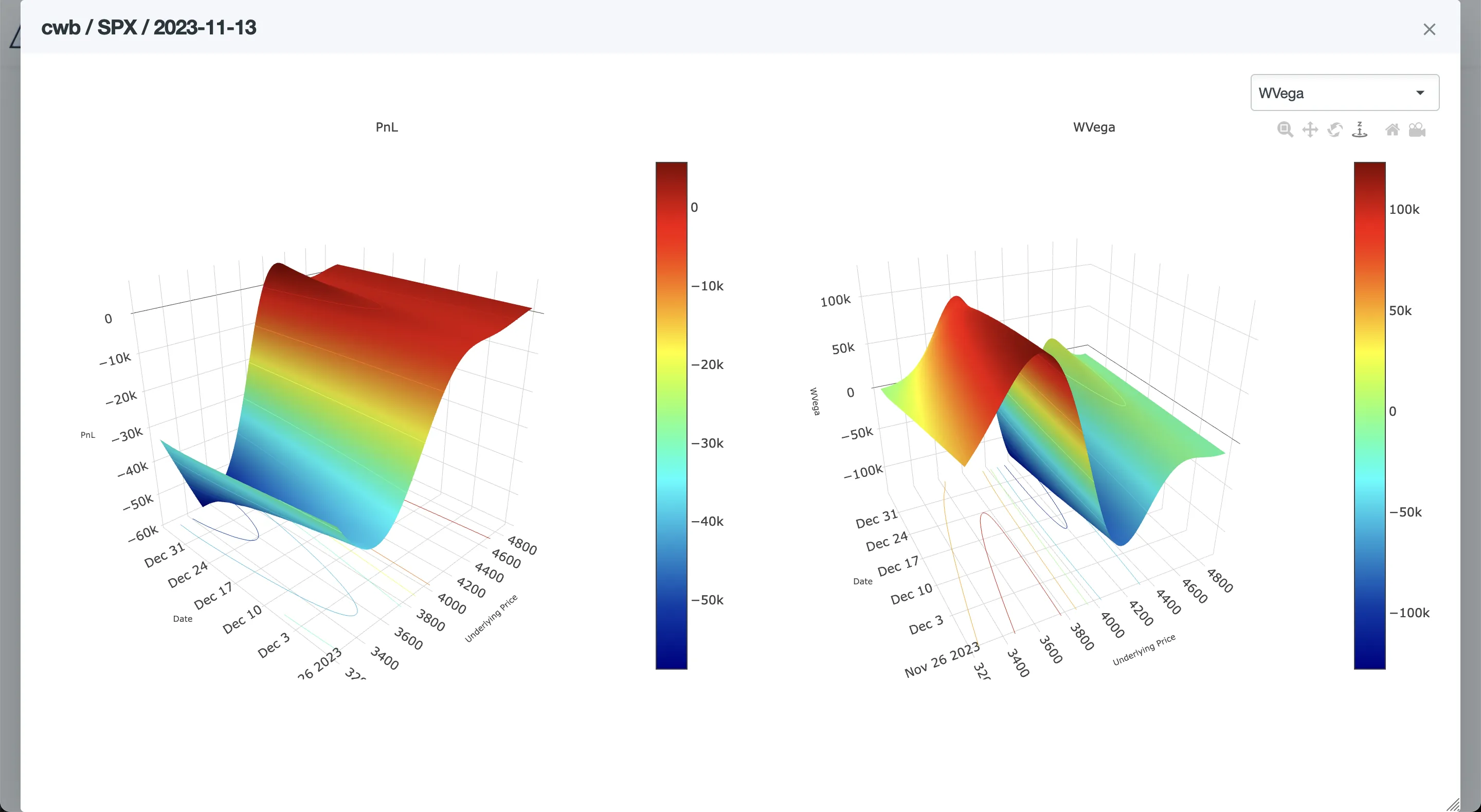

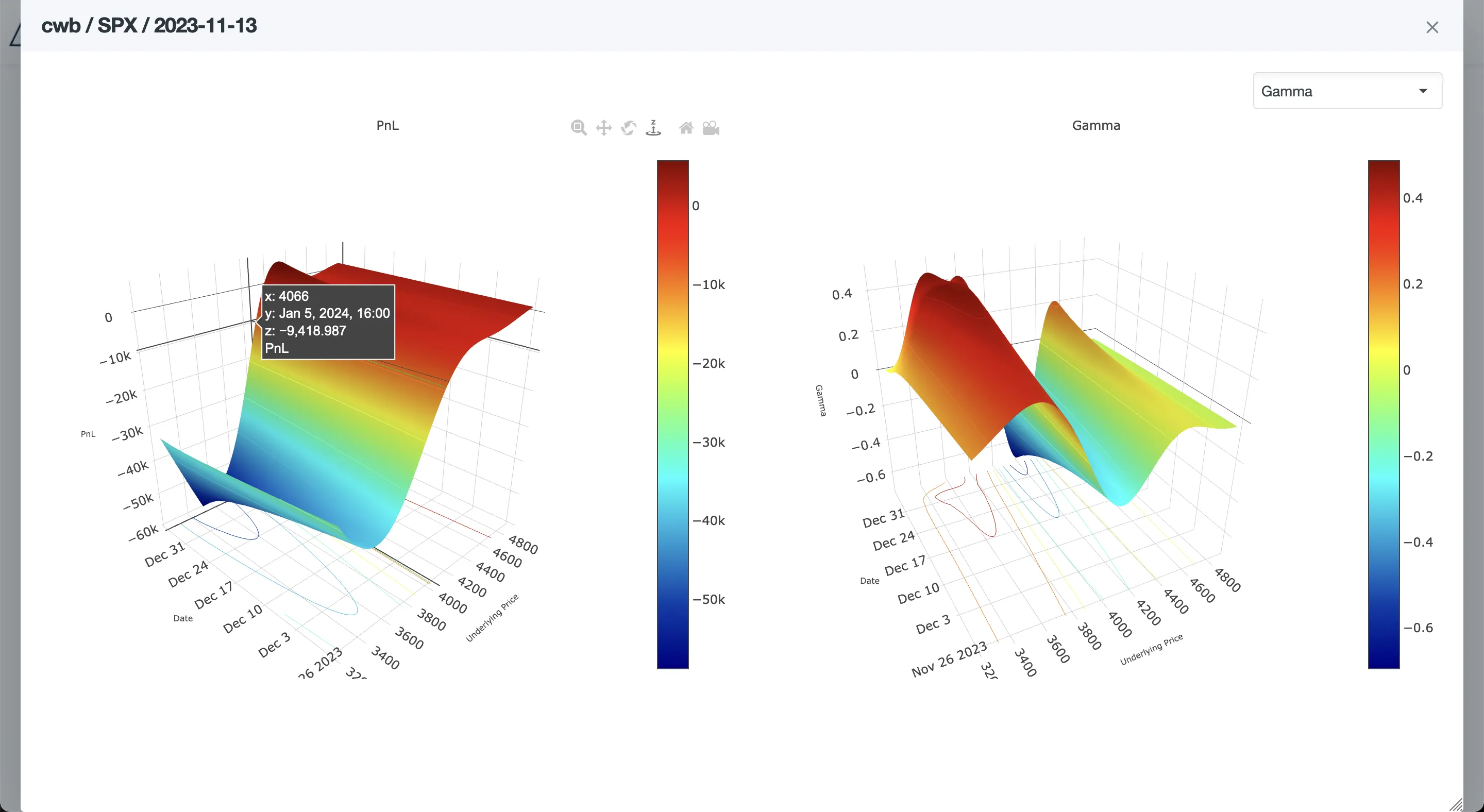

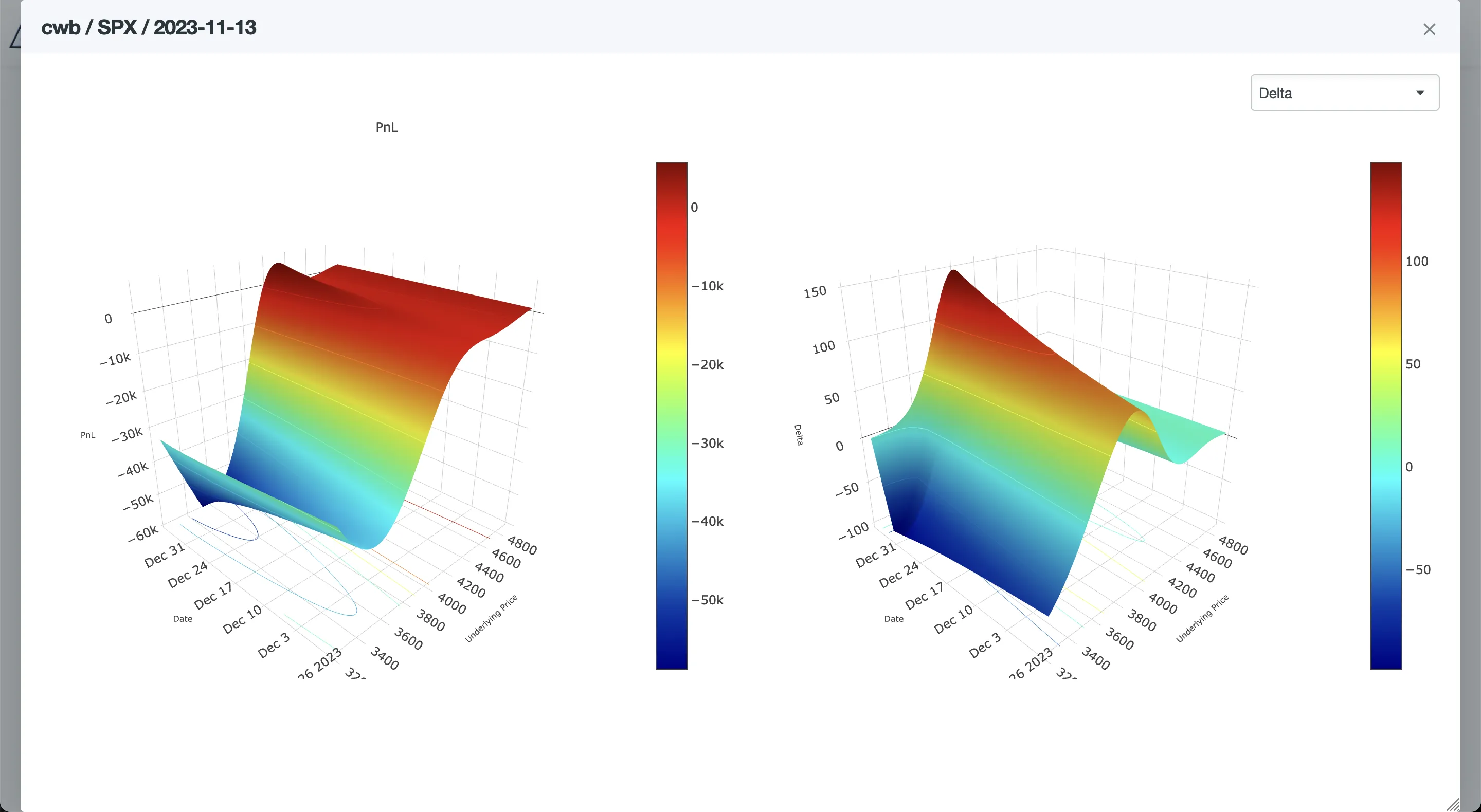

To fully address the “Limited information on Greeks” part we utilize 3D charts to display the changes in Greeks and PnL throughout the trades lifecycle. These graphs are useful to better understand the trade characteristics of position.

For open positions we show the PnL for both At Bid/Ask and at the Mark/Mid price level.

The monitoring capability of MesoLive is still a Work in Progress, but we believe it is already providing value compared to the currently existing solutions.

Execution

Some might think that once a trade plan is made the hardest part is over. While this is true, our experience shows that a lot of risk is present during execution. Sometimes it is hard to precisely follow the trade plan, due to:

- Time constraints: you might not always be available to enter / exit or adjust

- Mistakes: wrong contract selection can happen even with the best

- Negligence: hopium is a hard drug

These points will be addressed by MesoLive by taking MesoSim’s Strategy Definition and turning a backtest into a live trading job. We still believe that a full hands-off mode is risky with options trading, therefore it is not our goal to develop a fully automated system here. We might revisit this decision later.

The workflow we propose for executions (Entry / Adjustment / Exit) is as follows:

- Initiated from MesoLive

- Legs are automatically selected, and order is prepared

- Order is reviewed and submitted by the user

This part of MesoLive is not ready yet, but it is the next big work item in our roadmap.

We’ll take an iterative approach: Exits, Entries then finally Adjustments will be implemented.

Accuracy, Security, and Costs

While the three items in the heading seem distinctly related, they are actually defining our software architecture. Here is why:

-

Realtime data is expensive, especially for professionals and businesses.

Delayed data is unfeasible for trading, unless you do “buy and hold with monthly rebalances” type of strategy.While it would be easy and pleasant to develop a solution using data feeds from Exchanges or Data Vendors, it would make the price of the offering unfeasible for retail.

-

Security is of very high priority when it comes to handling money.

Storing access keys to brokerage accounts comes with risks we wish not to take.

Additionally, the user must be in full control at all times managing their account.

Both of the points above are addressed with our model:

We’ve created an Agent application that is run by the user providing a bridge between their brokerage account, live data stream, and our system. The Agent is certified by trusted software vendors, such as Microsoft and Apple. The Agent uses secure communication channels with tamper-proof keys to bring in account and realtime data to our systems. It is resilient to network failures and uses minimal system resources. The user is in full control of running this application.

Availability and price

MesoLive has been undergoing private beta for some time now with IBKR accounts.

We’re onboarding customers have shown interest in small groups on a weekly basis.

Currently, IBKR TWS is the only supported platform; additional brokerages may be supported later.

We consider the Position Monitor part to be 80% ready and expect to start the execution-related tasks immediately. As MesoSim provides a rich set of tools, reaching feature parity between Sim and Live is likely to be some quarters ahead.Since the offering is fairly resource intensive it will not be free.

We are continuously improving its performance so that it can operate in a cost-effective manner. Therefore, it would be too early to put a price tag on the offering.

As MesoLive in its full form will take MesoSim Jobs to Live, it makes sense to consider it as a paid add-on to MesoSim. We might or might not release the monitoring part as a separate solution later. Execution without access to MesoSim plan is a definite no from our standpoint.

This article was originally written for MesoSim v2. The examples and terminology have been updated to match the MesoSim v3 Strategy Definition format. For details, see the MesoSim v3.0 release announcement and the v2→v3 migration guide. The performance metrics, described behavior, and referenced run results reflect the original v2 behavior. If you rerun the referenced strategies on MesoSim v3, results may differ slightly due to behavioral changes in the simulator.