These income strategies cover a wide range of moneyness and time to maturity.

Some stand out, others are just average and some are not performing well currently.

It is well known that diversification helps build better investments.In this article, we will explore how Equal Weighting and Modern Portfolio Theory might help improve investment performance.

🤖 We're Thrilled to Announce the Integration of ChatGPT with MesoSim, the Advanced Options Simulator!

As we continuously strive to provide our users with the most innovative and efficient tools in the financial technology space, the incorporation of MesoSim's Knowledge Base to ChatGPT represents a major advancement in how you can interact with our platform.

Enhanced User Interaction: ChatGPT's cutting-edge AI capabilities allow for a more intuitive and conversational user experience. Whether you're querying complex options strategies or seeking help with Strategy Definitions, ChatGPT is here to assist you in plain language.

Personalized Support: Get instant, AI-driven answers to your queries without waiting. From explaining the Greeks in options trading to offering step-by-step simulation guidance, ChatGPT tailors its support to your unique needs.

Education and Insights: Alongside its support functionalities, ChatGPT serves as an educational companion, offering explanations, tutorials, and valuable insights to enrich your trading knowledge and decision-making.

Continuous Improvement: The integration is just the beginning! We're committed to evolving the platform's capabilities, ensuring that MesoSim remains at the forefront of technological innovation in the trading world.

Get Started: Dive into a seamless, smarter trading experience today. Engage with ChatGPT on MesoSim and explore the enhanced possibilities at your fingertips.

Thank you for being a part of our journey. We're excited to embark on this new chapter with you, pushing the boundaries of what's possible in options simulation. Your feedback is invaluable to us as we work to make MesoSim your go-to platform for all things options.

Disclaimer

While ChatGPT can now create MesoSim Strategy Definitions, it may suggest strategy definitions that do not fully capture the specified trade. Additionally, it might omit optional fields, leading to warnings in the Strategy Editor. Most of the time, these warnings can be safely ignored.

This article was originally written for MesoSim v2. In MesoSim v3, the agent is now called the MesoSim AI Assistant, and the always up‑to‑date entry point is available directly from the MesoSim portal via the AI Assistant navigation menu.

We are pleased to announce the release of MesoSim-v2.11. This release represents the most significant update to our codebase to date,

encompassing over six months of R&D work.

New features include:

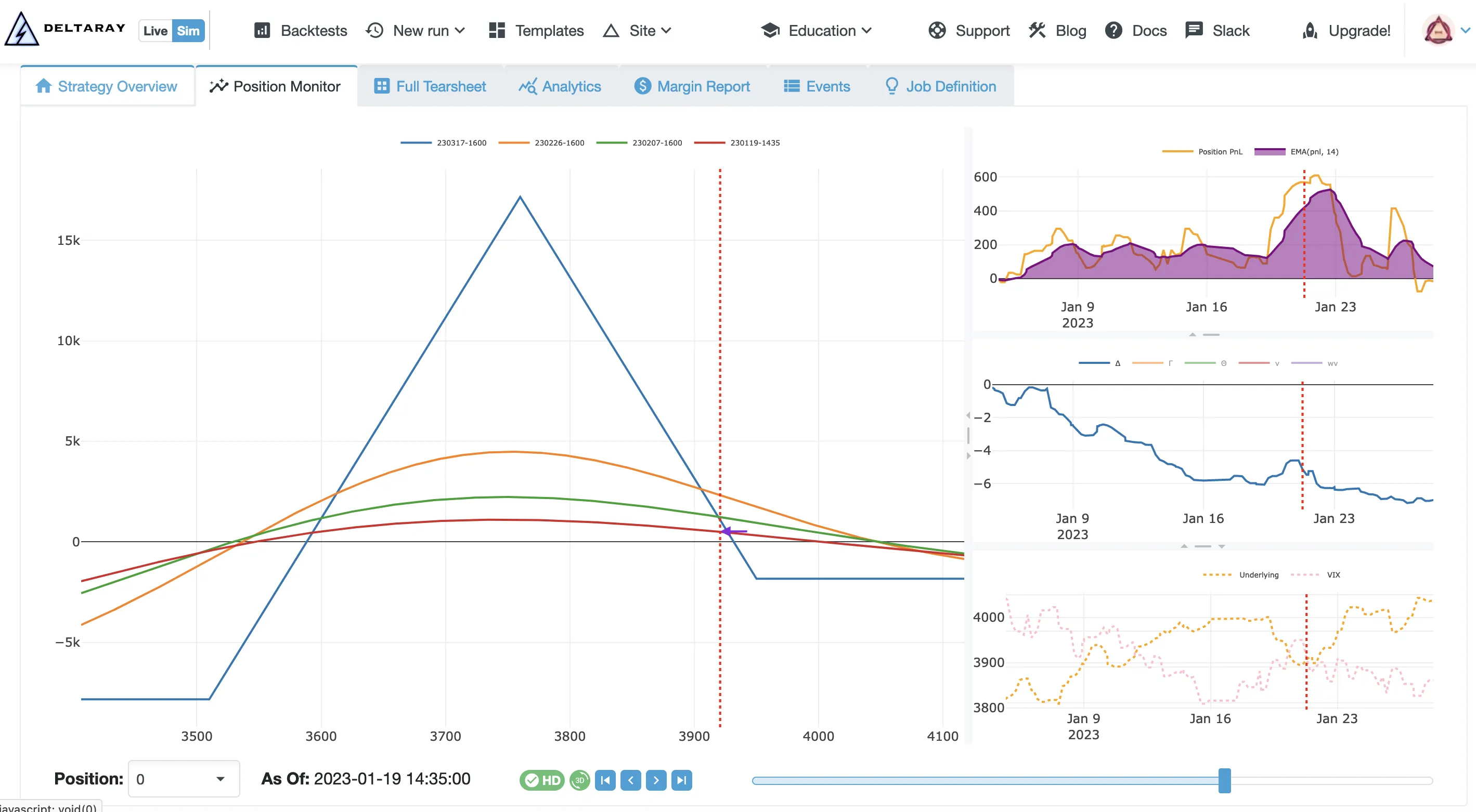

Backtest Position Monitor with high-accuracy Risk Graphs

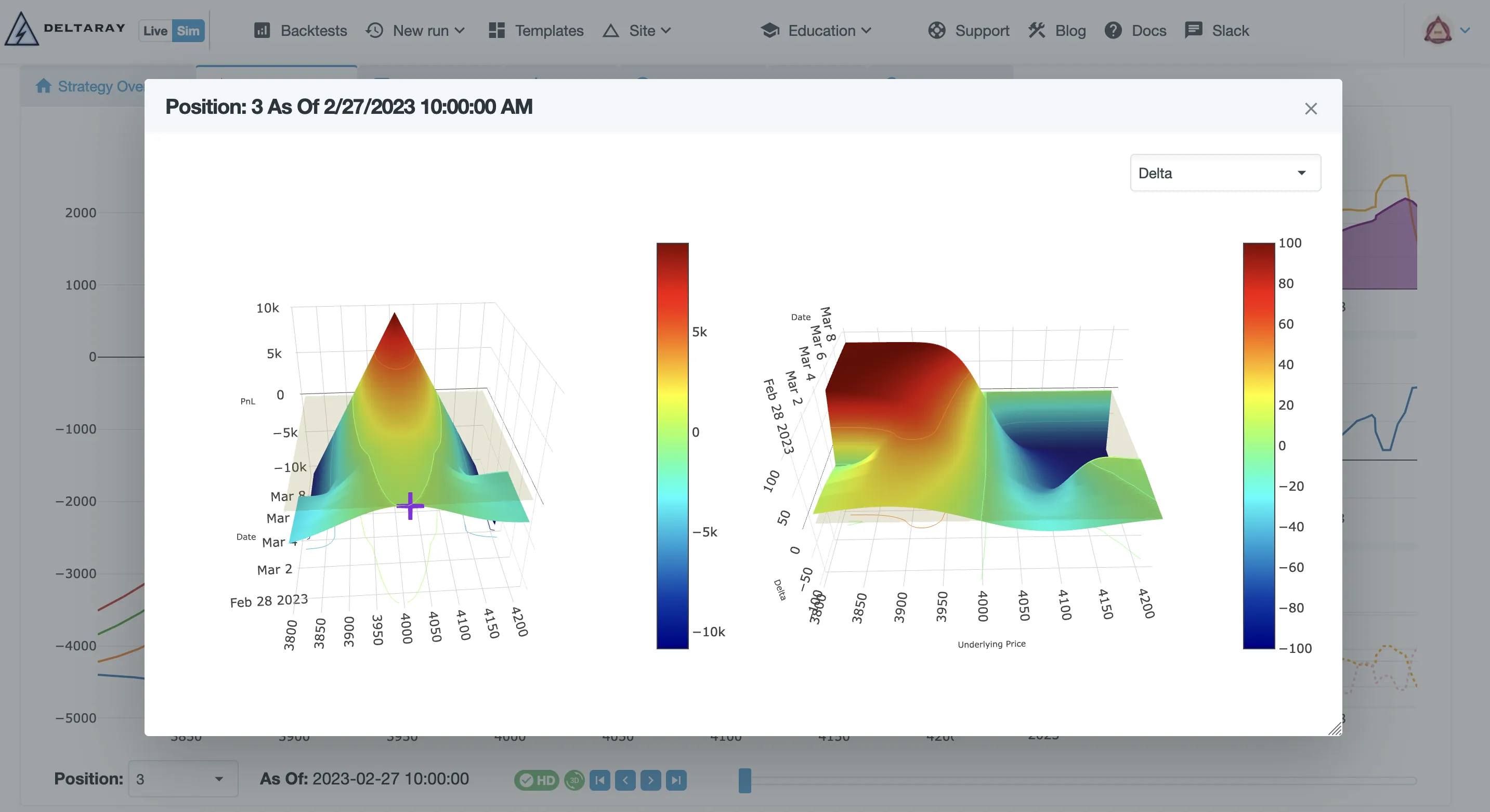

The Backtest Position Monitor, the first feature backported from MesoLive - our live offering - provides an accurate Risk Graph along with time series of PnL, Greeks, SPX, and VIX prices.

The Risk Graph Projection utilizes BQL - our proprietary extension of QuantLib - to deliver unparalleled accuracy in modeling both short- and long-dated options. We employ the Black-Scholes-Merton (BSM) model and tackle critical yet frequently overlooked challenges:

the impact of weekends and business holidays and the determination of the risk-free rate.

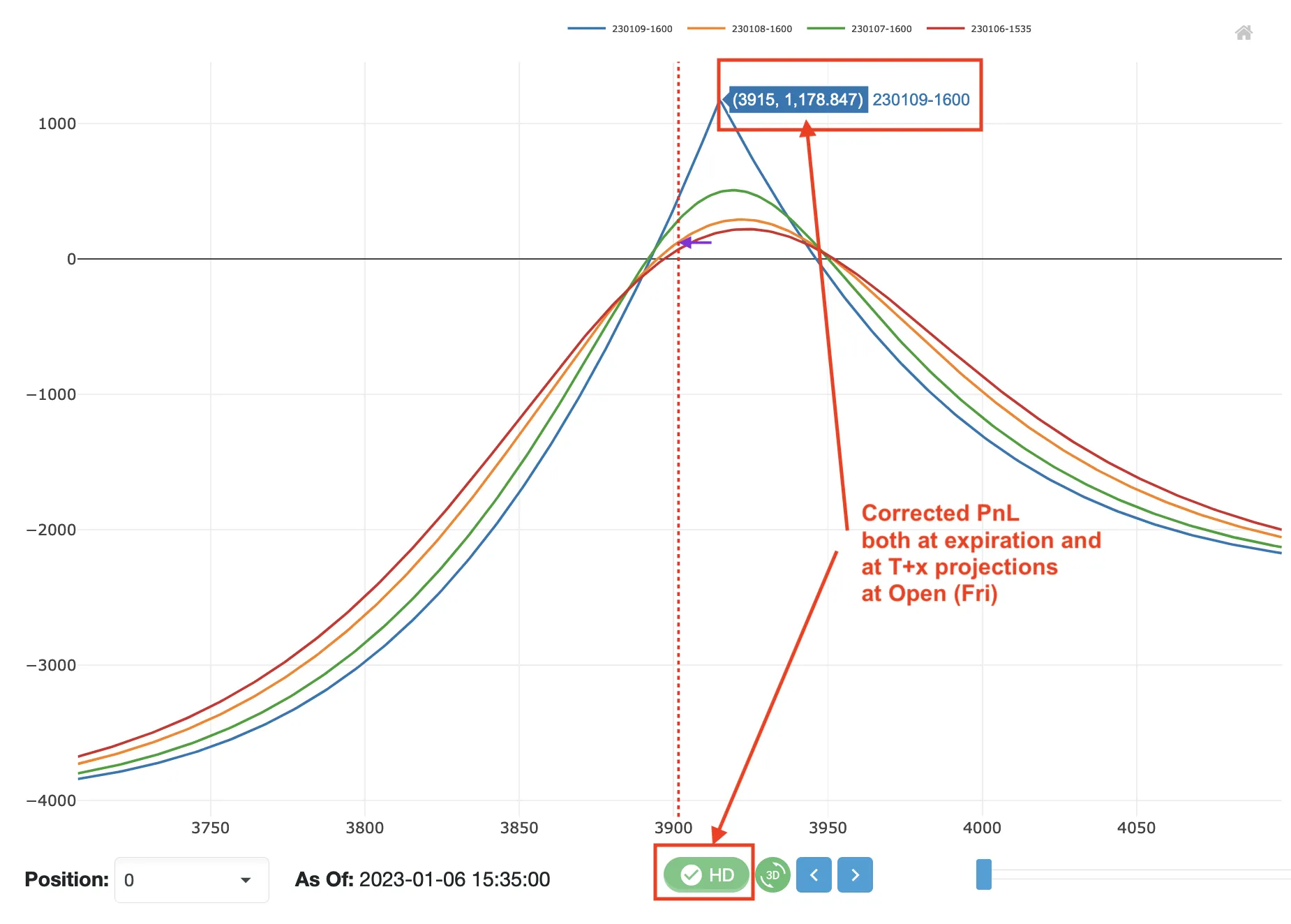

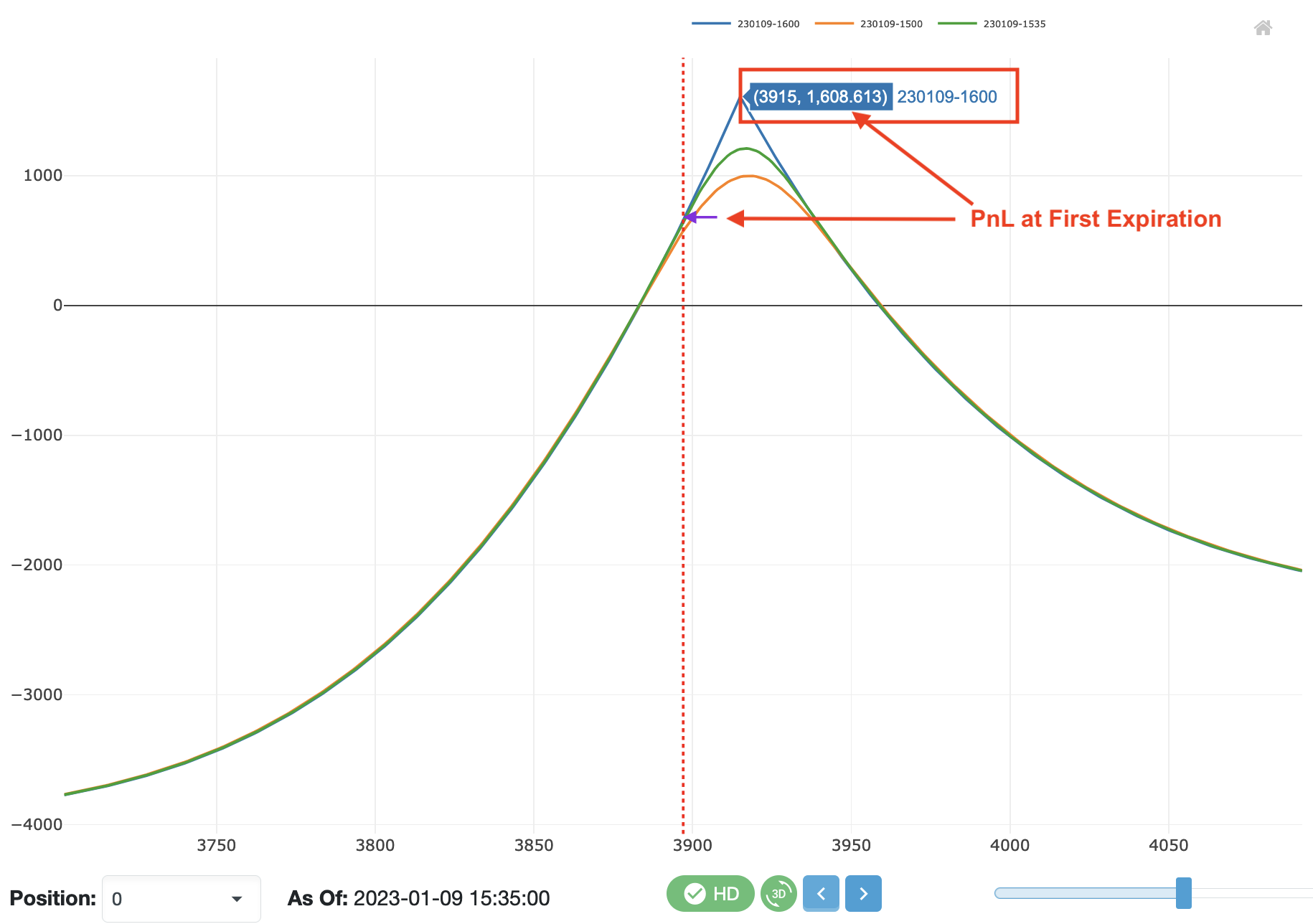

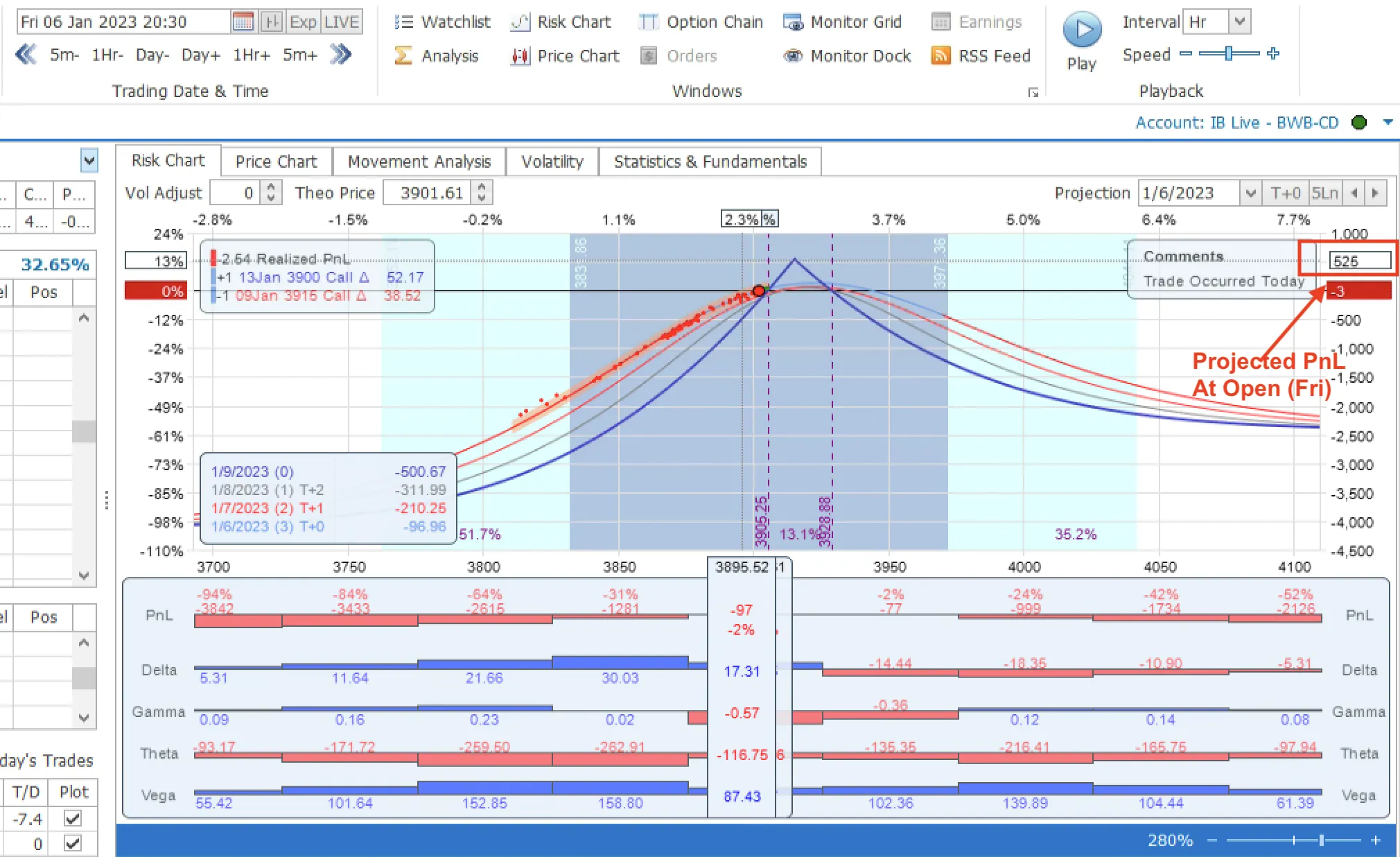

Have you ever tried to project the payout of short-dated options that span over a weekend? You might have noticed that the Risk Graph drastically changes from Friday to Monday in traditional modeling software. This is because the implied volatility (IV) on Friday accounts for the weekend, a time when markets are closed but market-moving events can still occur. With HD mode enabled, we adjust the IVs to provide a more accurate projection in MesoSim.

As the screenshots demonstrate, OptionNet Explorer (among others) tends to underestimate the payout for the outlined scenario. When HD mode is disabled, MesoSim’s Risk Graph resembles those of lower-resolution modeling tools.

The BSM Model requires the number of days until expiration to be provided. While most implementations utilize Calendar Days, it's important to note that US Index Options are tradable only on business days. To improve accuracy, we use a Business Calendar that accounts for weekends, market holidays, and early closures.

The risk-free rate is an essential input parameter for the BSM model. While US Treasury bills (T-Bills) are commonly used as a simple proxy for the risk-free rate, more accurate results can be achieved by extracting (bootstrapping) the risk-free rate from option chains. This extraction can be performed using Box Spreads, where we establish a synthetic long and a synthetic short position at

the same set of strikes within the same expirations. For European options, the payout will reflect the actual risk-free rate as implied by the option contracts.

We calculate thousands of Box Spreads to derive a stable measure for each expiration. We then apply the expiration-specific risk-free rate to project the PnL for the position in question.

Accurately determining the risk-free rate is particularly crucial for longer-dated options and has become

increasingly relevant as we move away from the zero interest rate policy (ZIRP).

Traditional 2D risk graphs are commonly utilized to illustrate the risk profile of a position. However, due to their format, it is impractical to depict drastic changes (e.g., when a contract expires) in the projection or to demonstrate how the Greeks change over time. To overcome these limitations, we have introduced 3D graphs that display both the PnL projection and the Greeks throughout the entire lifecycle (until the last expiration) of the position.

To capture the Risk Graphs, you must enable Trace Collection through Settings.Sim.PositionMonitor. Once enabled, the information will be displayed in the Position Monitor tab of a completed backtest.

We are proud to announce that Risk Graph generation is fast!

It can sustain a rendering performance* of 24 frames per second on modern cloud hardware, enabling you to navigate through frames with minimal to no delay.

*: for a three-legged options structure using one expiration

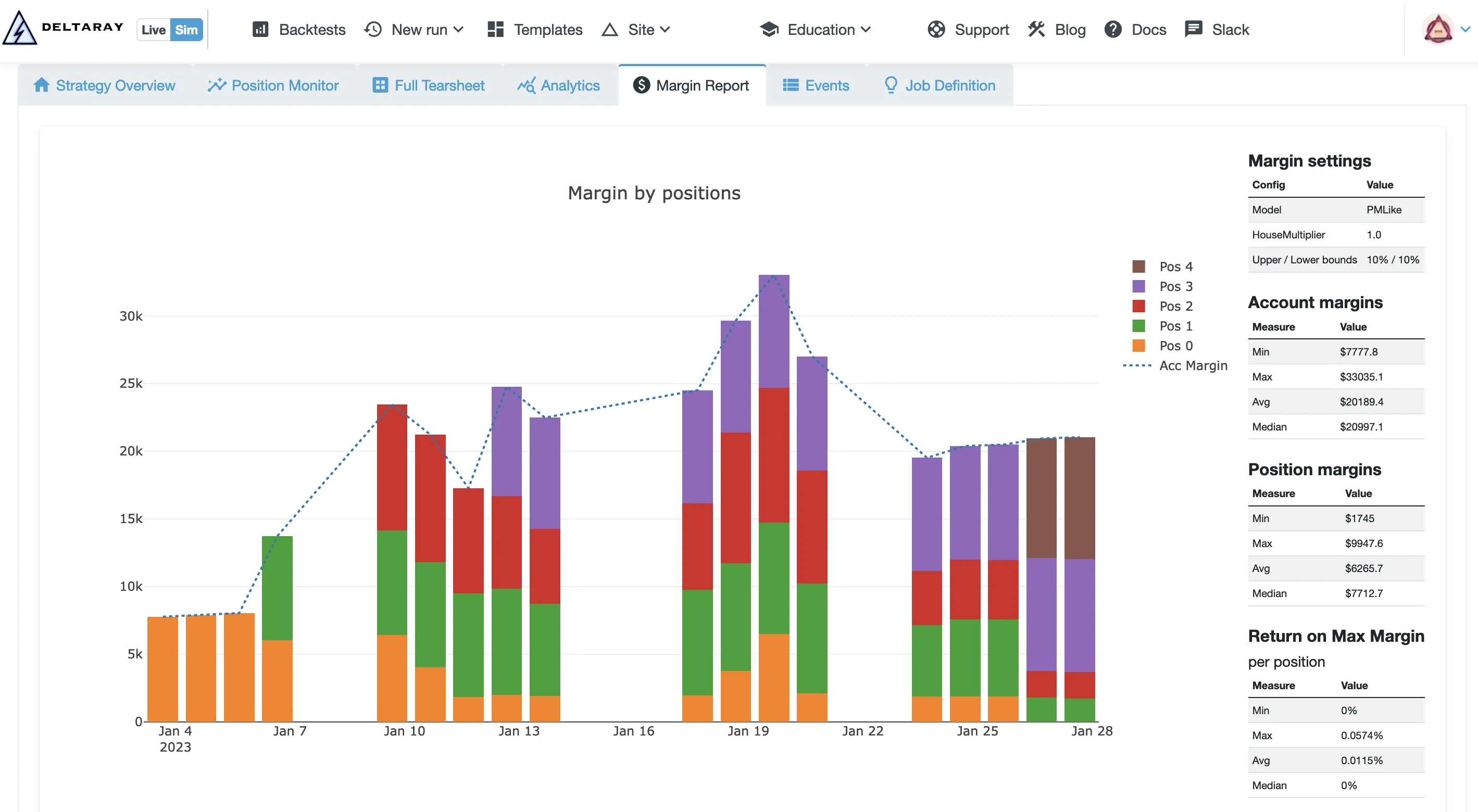

In MesoSim-v2.8, we introduced Regulation T margin, which has now been enhanced with a model similar to the Portfolio Margin used by brokerages. We utilize the technology behind Risk Graphs to approximate Portfolio Margin requirements using User-Specified configurations (including haircut levels).

As with RegT margin, the calculations are made accessible to the user via the pos_margin variable.

Margin enhancements are available in our Advanced and Academia plans.

We obtained VIX data from the CBOE some time ago. During the ingestion process, we noticed inconsistencies in some of the Greeks, leading us to label the VIX data as beta. After extensive discussions with the CBOE, they revised their models and provided us with an updated dataset. With the most recent update, the issues we identified have been resolved, and we are pleased to announce that the VIX data is now classified as stable in MesoSim.

note

VIX, along with RUT, is available in our Advanced and Academia plans.

We trained ChatGPT to know about MesoSim semantics to reduce the barrier of entry!Head to the dedicated post to learn more about this offering or try to use it directly.

We have added two variables to expose the Bid and Ask prices of the legs at any given time. These Bid/Ask prices can subsequently be utilized in all Lua fields.

By exposing the Bid/Ask prices, one can configure the Exit Conditions so that a position is exited only when both prices are present.

We would like to thank all the MesoLive and MesoSim beta testers who helped to craft the Position Monitor. We're extremely grateful for AKJ’s insights regarding the accuracy of the Black-Scholes-Merton Model!

We are actively working on MesoSim’s Optimizer, which will be available in the FundPro Plan. In addition, we plan to enhance the Documentation and Education sections of our site.

Furthermore, development of MesoLive continues as well.

MesoSim v3 Migration Note

This article was originally written for MesoSim v2. The examples and terminology have been updated to match the MesoSim v3 Strategy Definition format. For details, see the MesoSim v3.0 release announcement and the v2→v3 migration guide. The performance metrics, described behavior, and referenced run results reflect the original v2 behavior. If you rerun the referenced strategies on MesoSim v3, results may differ slightly due to behavioral changes in the simulator.