Volatility Hedged Theta Engine

We have previously covered David Sun’s (@thetradebusters) Theta Engine in one of our blog posts. The power of Theta Engine comes from David’s unique method for determining the size of short put positions. For more details on his approach, please refer to our blog post and his website.

About the variant

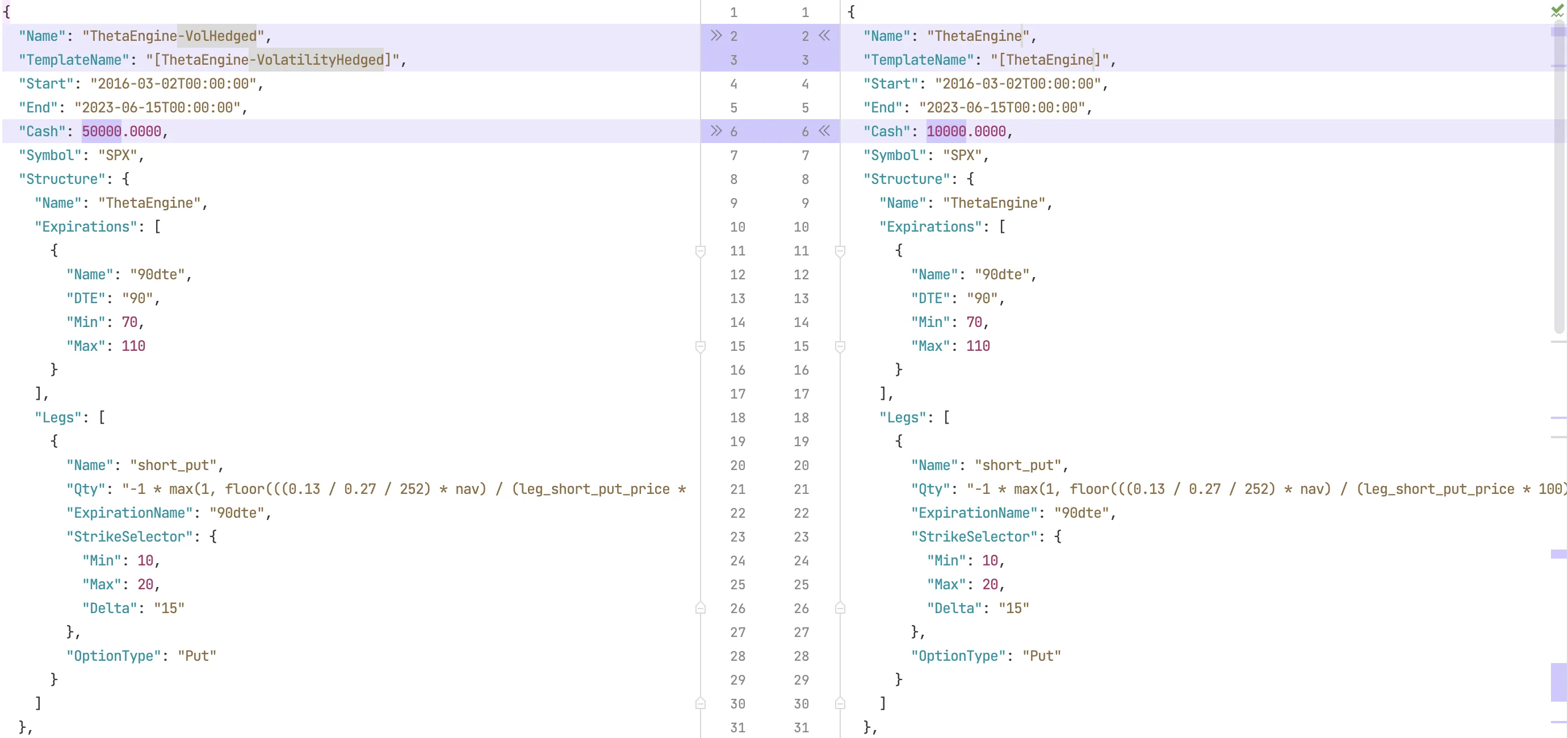

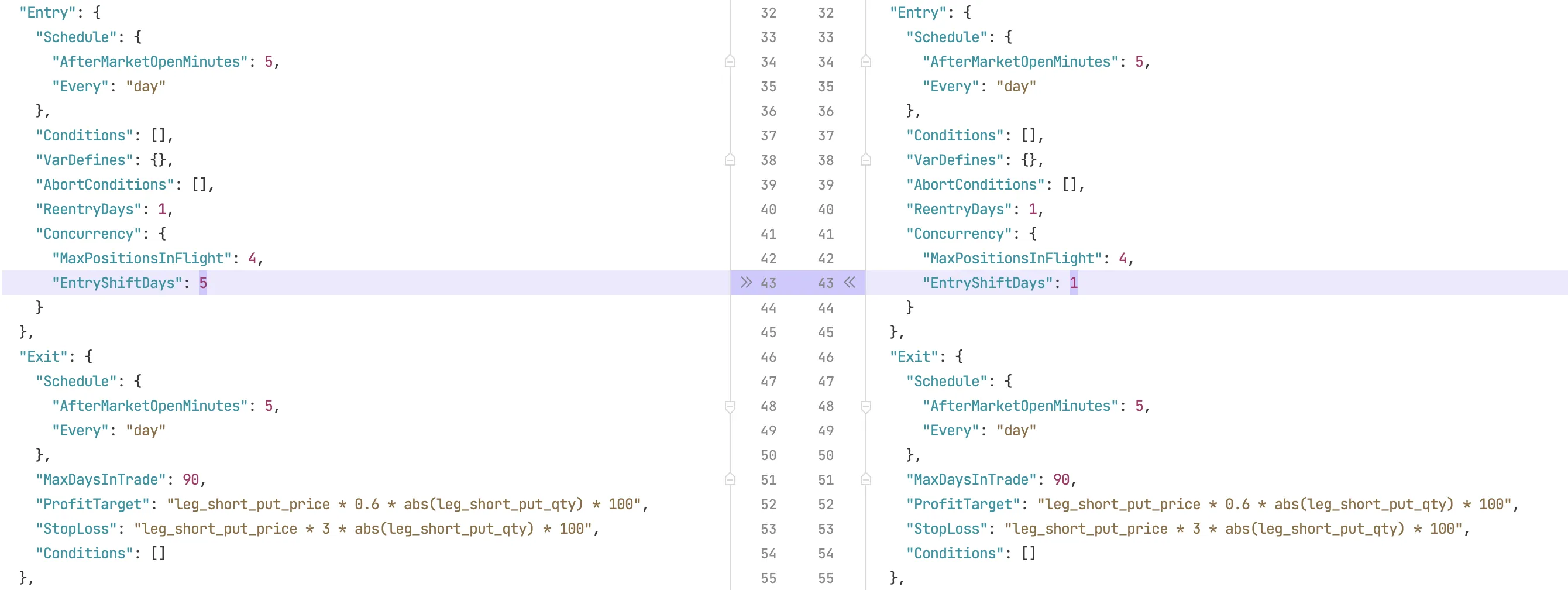

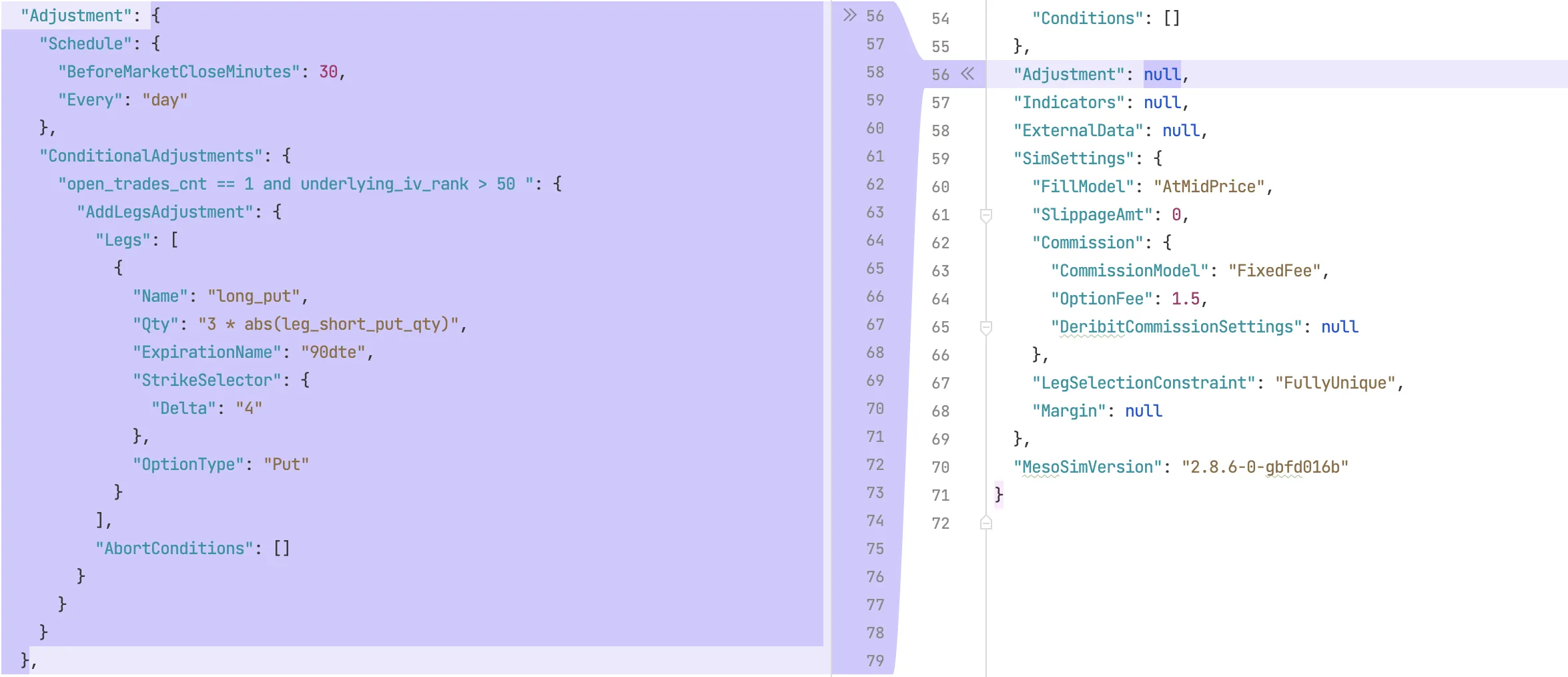

Claudio Valerio, a valued member of our community has created and shared a variant of the Theta Engine strategy. His modification includes a dynamically added long put hedge during periods of elevated Implied Volatility (IVRank > 50). He selects the contract closest to Delta=4 with the same expiration as the short put. The number of purchased contracts is three times the number of shorts sold. Additionally, Claudio has adjusted how the parallel positions are spread out and increased the planned capital of the trade.

Volatility based Hedging

IV Rank is used to define two regimes for the market.

Low volatility regime

When the ATM Implied Volatility for SPX Options is below the mid point of its 52 week high-low range (IVRank < 50), we go with naked shorts as the original trade did.

Elevated volatility regime

When IVRank reaches (or goes beyond) 50, then 3x as many longs are added as shorts, creating a 3:1 Put Ratio Backspread. With the added hedge he is substantially reducing the downside risk and capping the upside profit potential.

Note on hedging

While ThetaEngine originally does not contain a hedging component, David has shared his hedging strategies (Vibranium Shield and Bomb Shelter) in great detail. Hedging is a must when it comes to selling options, therefore we suggest that you study David’s original hedges or Claudio’s variant with the built-in hedge. It shall be noted that while reactive hedging (as presented here) is a cost-efficient way, it will likely not provide good coverage for scenarios where the market is closed and crashing, such as during the 9/11 events.

Differences

The following section shows the two trades side-by-side.

Strategy Definition

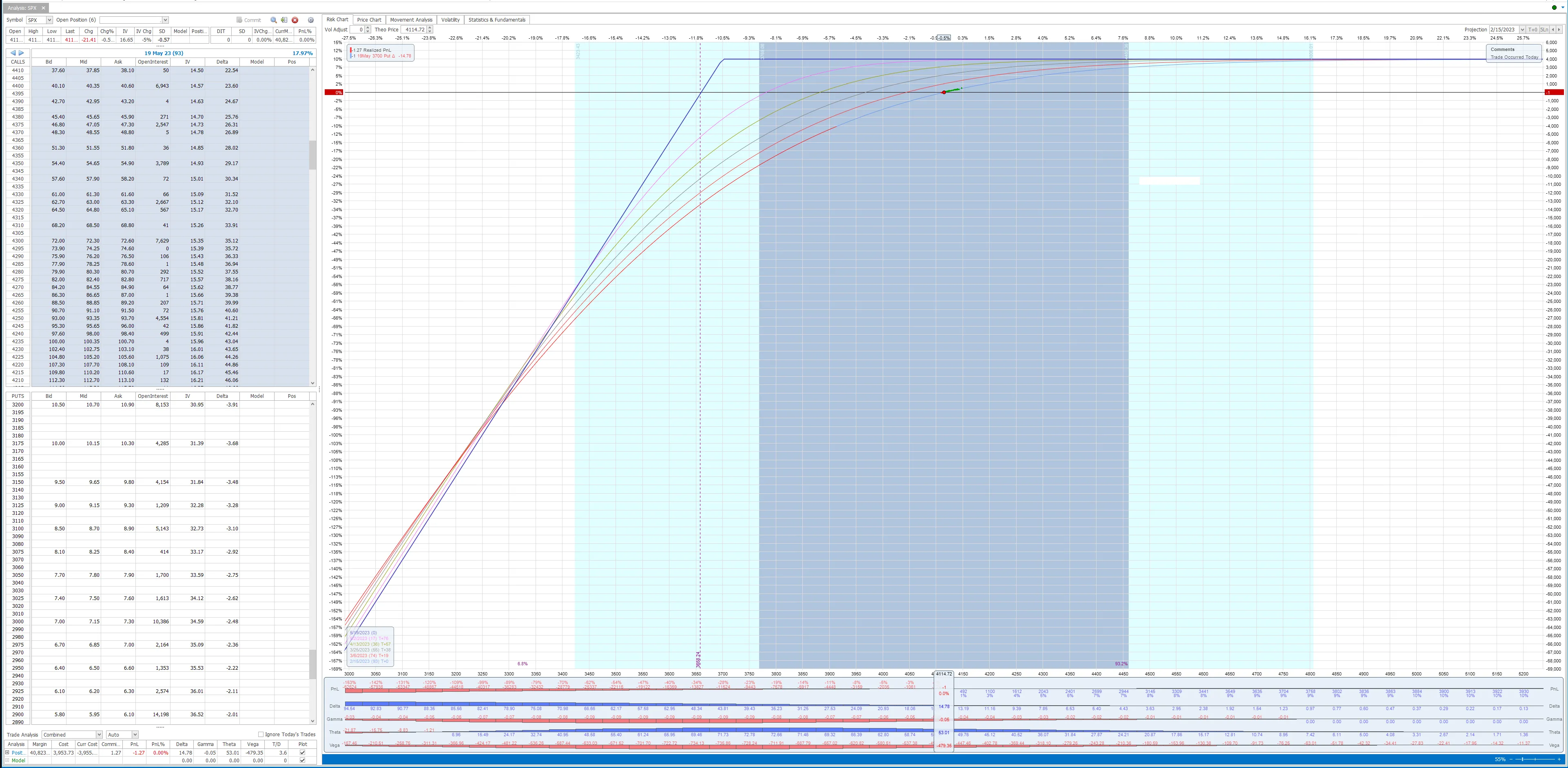

Risk Graph

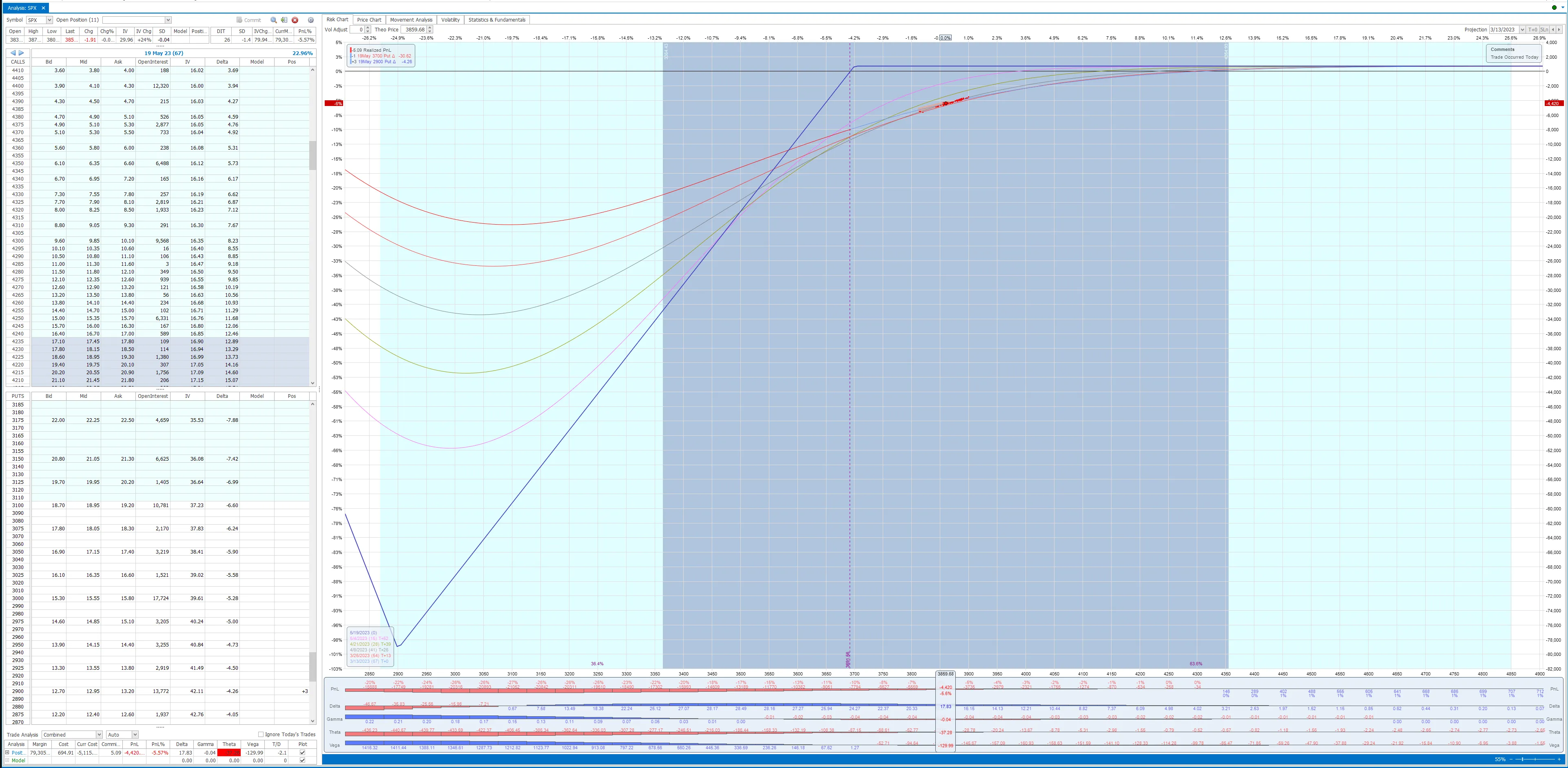

To study the characteristics of the trade we'll be using OptionNet Explorer. The following two screenshots are showing the Risk Graph when the position is naked short and when the hedge is added.

About sizing:

MesoSim’s built-in ThetaEngine template is more aggressive (details in the ThetaEngine post) than David’s original trade plan. Claudio has taken our built-in template with 25% credit target and created his variant allocating $50k for the trade.

Thanks

We would like to thank Claudio for sharing the Volatility Hedged Theta Engine and David for creating the original trade plan!

This article was originally written for MesoSim v2. The examples and terminology have been updated to match the MesoSim v3 Strategy Definition format. For details, see the MesoSim v3.0 release announcement and the v2→v3 migration guide. The performance metrics, described behavior, and referenced run results reflect the original v2 behavior. If you rerun the referenced strategies on MesoSim v3, results may differ slightly due to behavioral changes in the simulator.