Risk Premium Harvesting with QuantPedia Composite Seasonality Index

The anomaly

Calendar effects/anomalies are well-known to investors.

QuantPedia's Composite Seasonality Index (QCSI) combines several, seasonal patterns such as the Turn of the Month, FOMC Meeting Effects, and Option-Expiration Week. It has been shown that using the composite calendar in a long-only setup outperforms the market.

Euan Sinclair also describes an Options Trading Strategy for FOMC events in his famous Positional Options Trading book. It's worthwhile to read!

MesoSim implementation

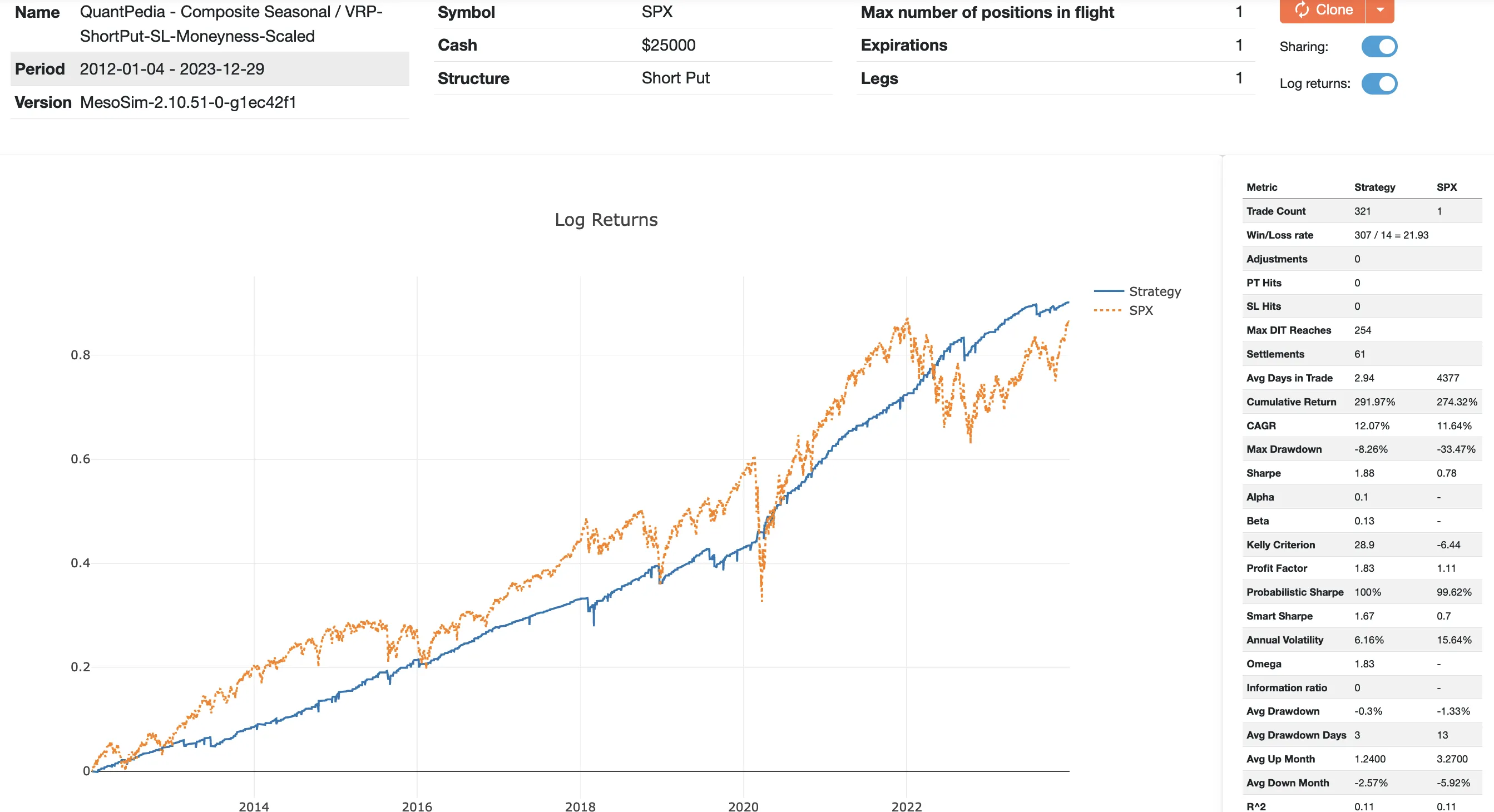

In a recent in-depth study, we investigated applying QCSI to Risk Premia Harvesting.

As the QCSI provides a bullish signal, we sell Puts at 10 Delta when the signal fires. We implement Stop-Loss trigger by comparing the selected contract's price with the underlying: the position is closed when the contract becomes In The Money (ITM).

These key market dates are provided via this Google Spreadsheet.

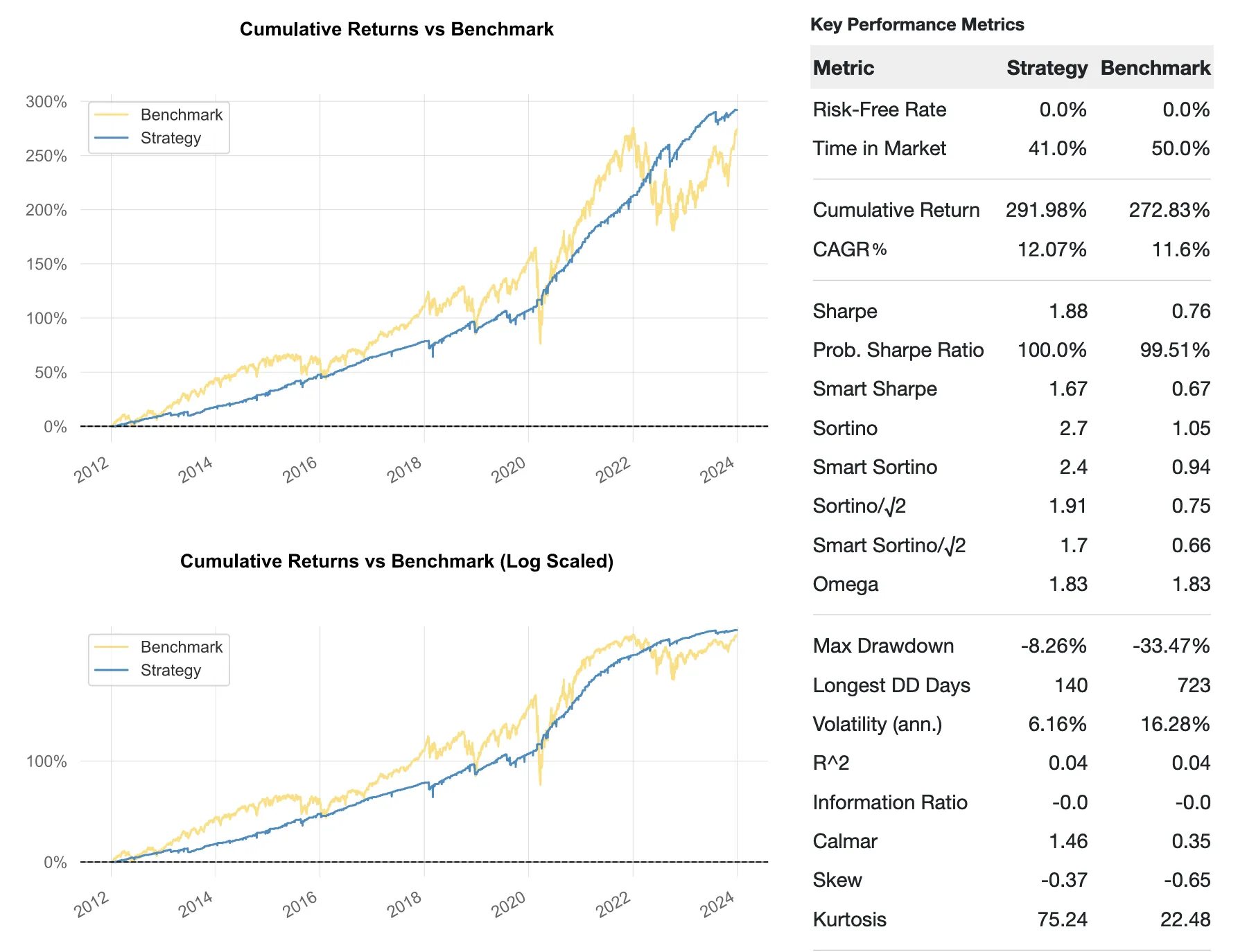

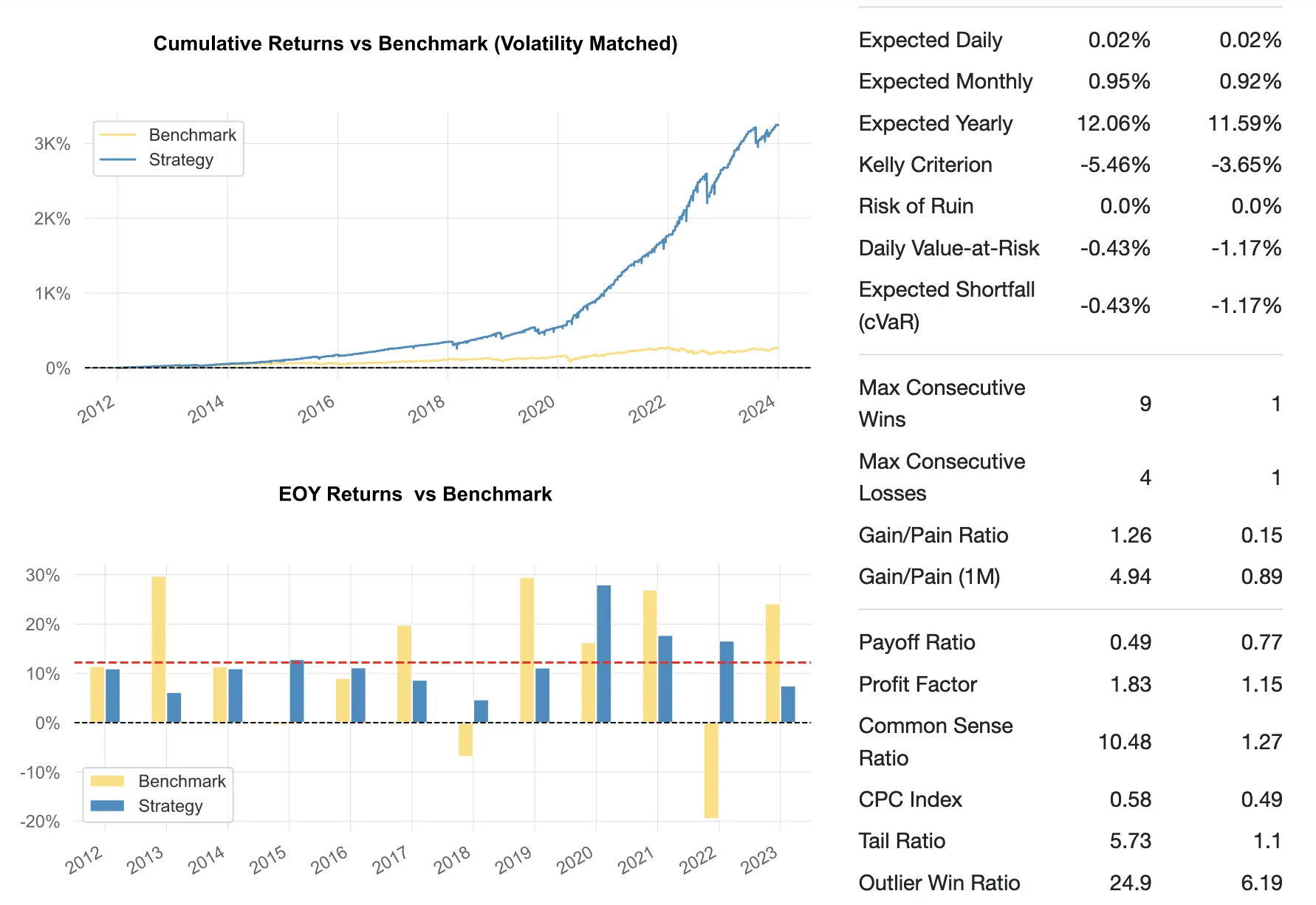

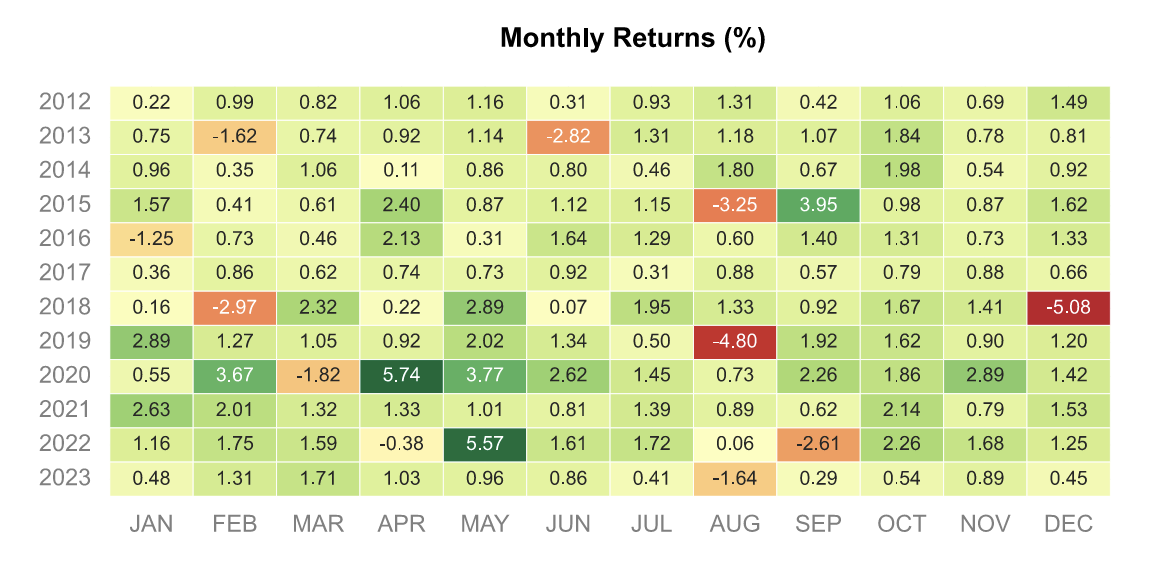

The backtest results can be viewed here.

Tearsheets

Results

Sharpe ratio for the 11 year test period is a notable 1.85.

The time in market is reduced to 40%.

To get all the implementation details, please read the full study on SSRN.