The Weekend Effect

In our next post in the series of options trading strategies on the public domain, we are presenting the Weekend Effect.

This trade (and others) has been discussed in detail in Euan Sinclair’s Positional Option Trading (Wiley, 2020) book. We highly recommend reading Euan’s books as he provides practical guidance on Options Trading in great detail.

Overview

The Weekend Effect in options refers to the tendency of options prices to decrease more over the weekend than in their respective weekday period.

Traders aware of the weekend effect can potentially profit by selling short-term options on Friday and buying them back on Monday at a lower price.

However, this strategy also comes with risks, such as unexpected market events that could cause a significant change in option prices over the weekend. Therefore, it is strongly suggested (mandatory) to pair this trade with a hedge. We will cover hedging strategies in a later article.

The validity of this hypothesis can be evaluated using MesoSim through a series of straightforward tests, which we are undertaking in the subsequent section of this article.

Trade Rules

The original trading rule is defined in Euan Sinclair’s book:

"On a Friday, sell the options that expire the next Monday."

Based on this guidance, our backtest trading rules are as follows:

- Find next Monday's or Tuesday's expiration

- Enter trades using the chosen expiration on Friday, 15 minutes before close

- Exit trades on Monday or Tuesday, 15 minutes after the open

The Tuesday expiration selection and Exit rules are present so that we can cover long weekends. In case of normal weekends, the Monday expiration and exit should be used.

For demonstrational purposes, we will be using short puts and strangles to showcase this trade. It should be noted though, that the strategy should work with more complex structures, such as butterflies and iron condors.

Short Put version

Strategy Definition

We set the strategy to enter a position on a Friday and exit on Monday by using the following conditions in the Strategy Definition.

In the Expirations section, we specify that expirations will be selected between three and four DTEs, targeting 3. This enables trades entered on Friday and kept until Monday or Tuesday (in case of a long weekend).

"Expirations": [

{

"Name": "exp",

"DTE": "3",

"Min": “3”,

"Max": “4”,

"Roots": null

}

]

The Entry schedule is set to enter the trade each Friday 15 minutes before market close, and the Exit set to exit the trade the next trading day, 15 minutes after the market opens.

"Entry": {

"Schedule": {

"BeforeMarketCloseMinutes": "15",

"Every": "fri"

},

...

},

"Exit": {

"Schedule": {

"AfterMarketOpenMinutes": "15",

"Every": "day"

},

"MaxDaysInTrade": "1",

...

},

The Strike Selection is done based on Delta, we simply pick a 10 delta put to avoid selling tail risk.

"Legs": [

{

"Name": "short_put",

"Qty": "-1",

"ExpirationName": "exp",

"StrikeSelector": {

"Min": "5",

"Max": "15",

"Delta": "10"

},

"OptionType": "Put"

}

]

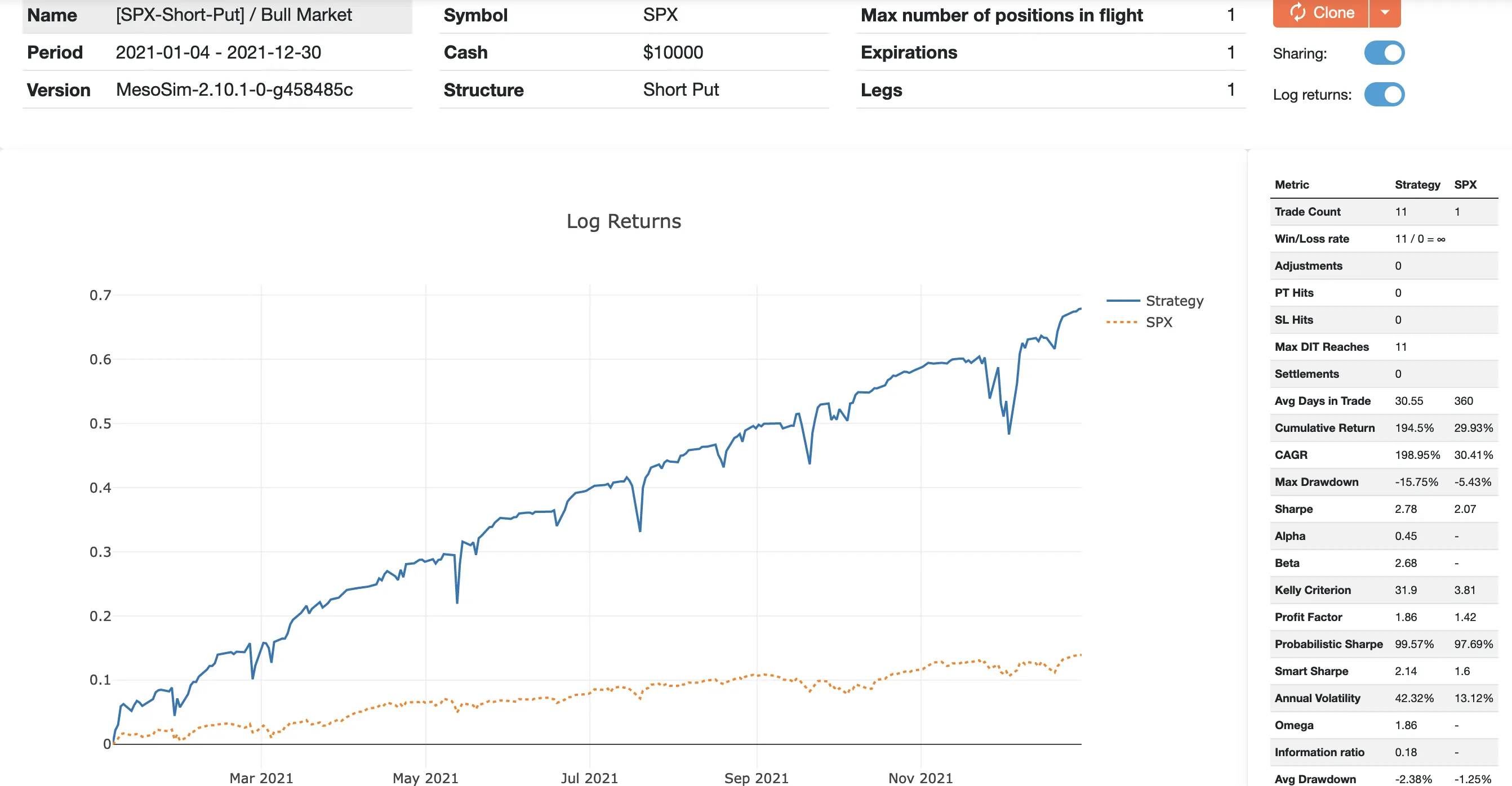

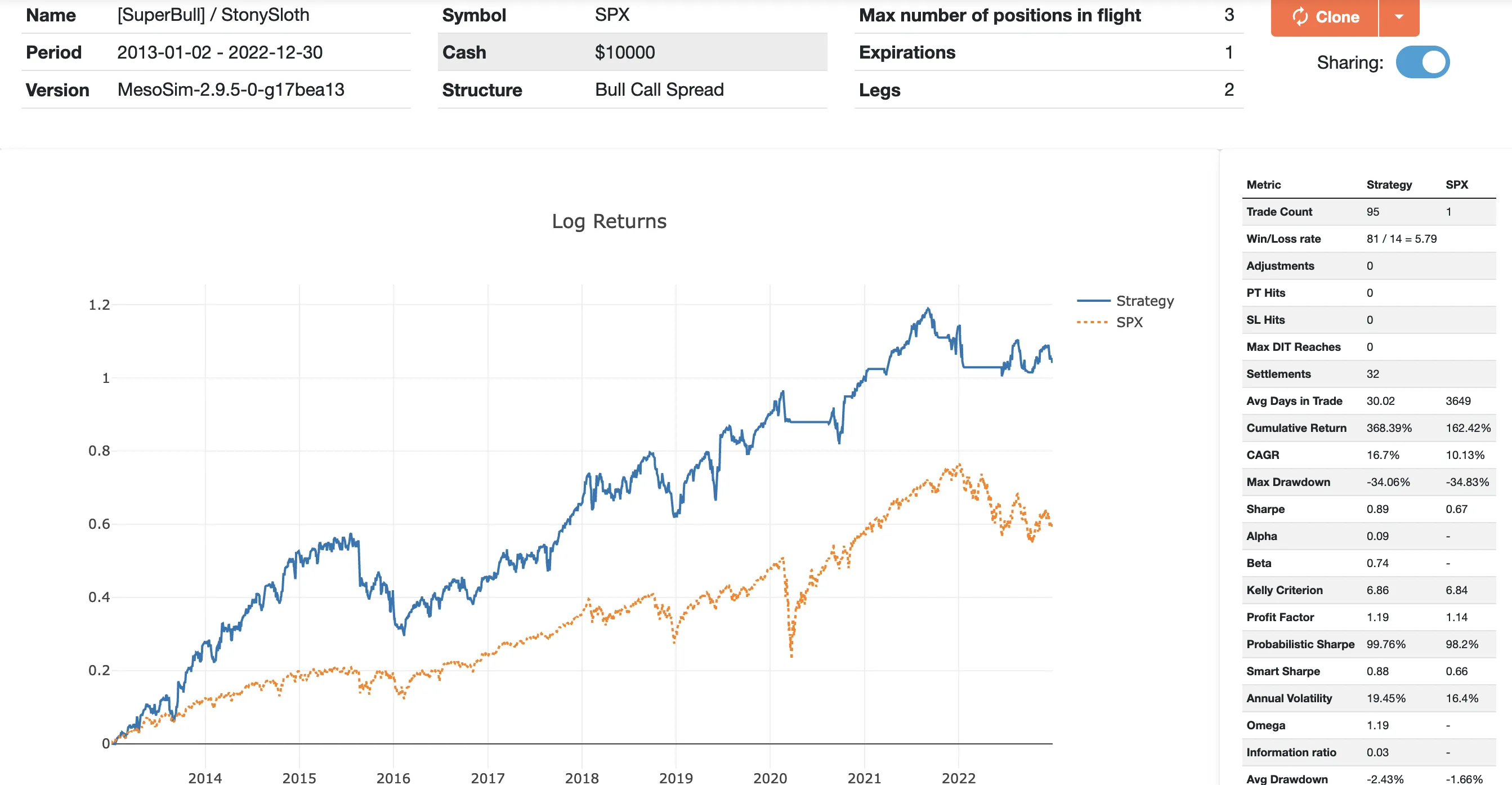

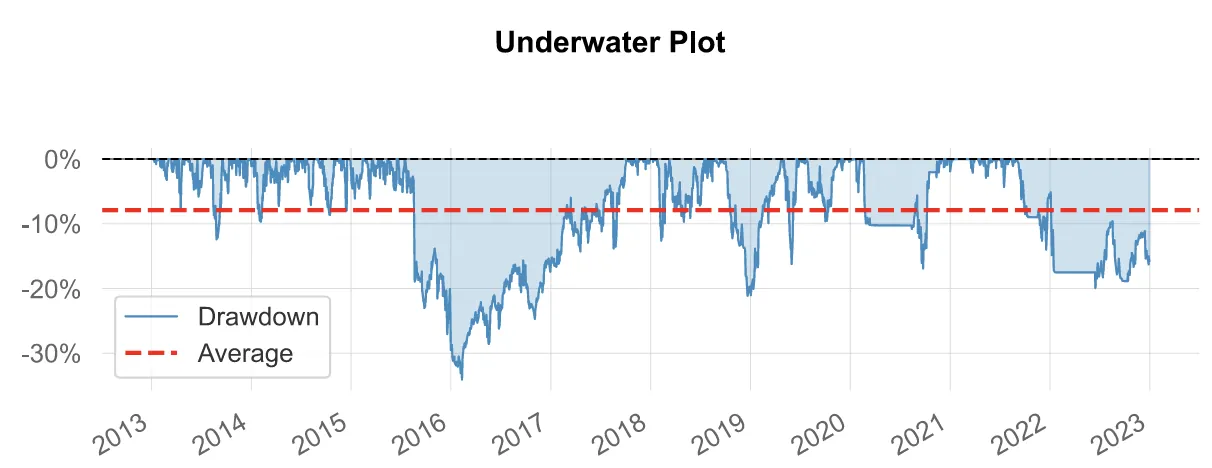

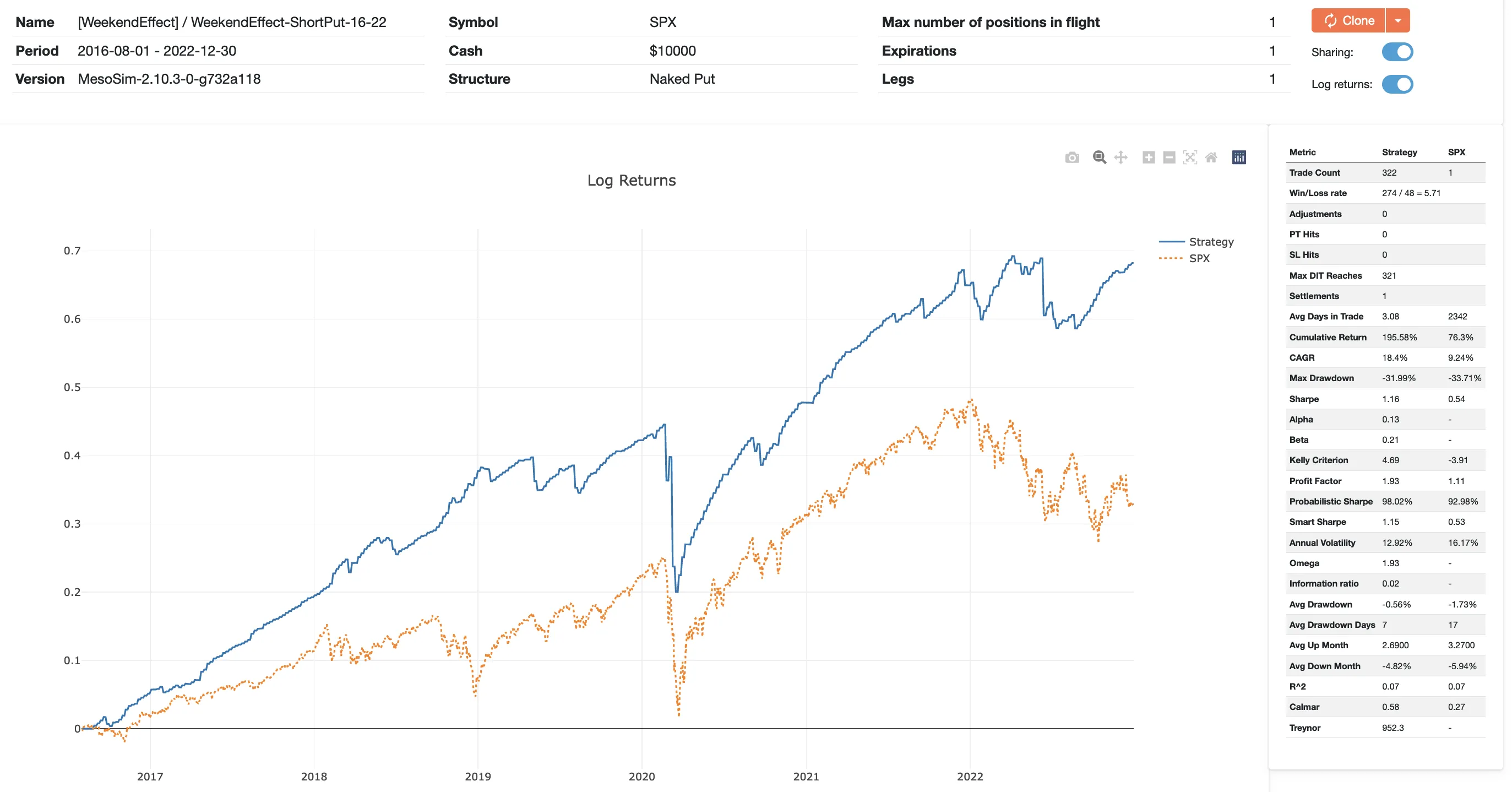

Backtest results: 2016 - 2022

Short Put - Friday to Monday

While we reduced the time spent in the market the returns are outperforming a simple S&P buy-and-hold strategy with a great margin: CAGR is doubled while the Max Drawdown stayed the same.

The full run with all the statistics is available at the following link: https://mesosim.io/backtests/755c4562-b166-490b-9295-74c36d56dc21

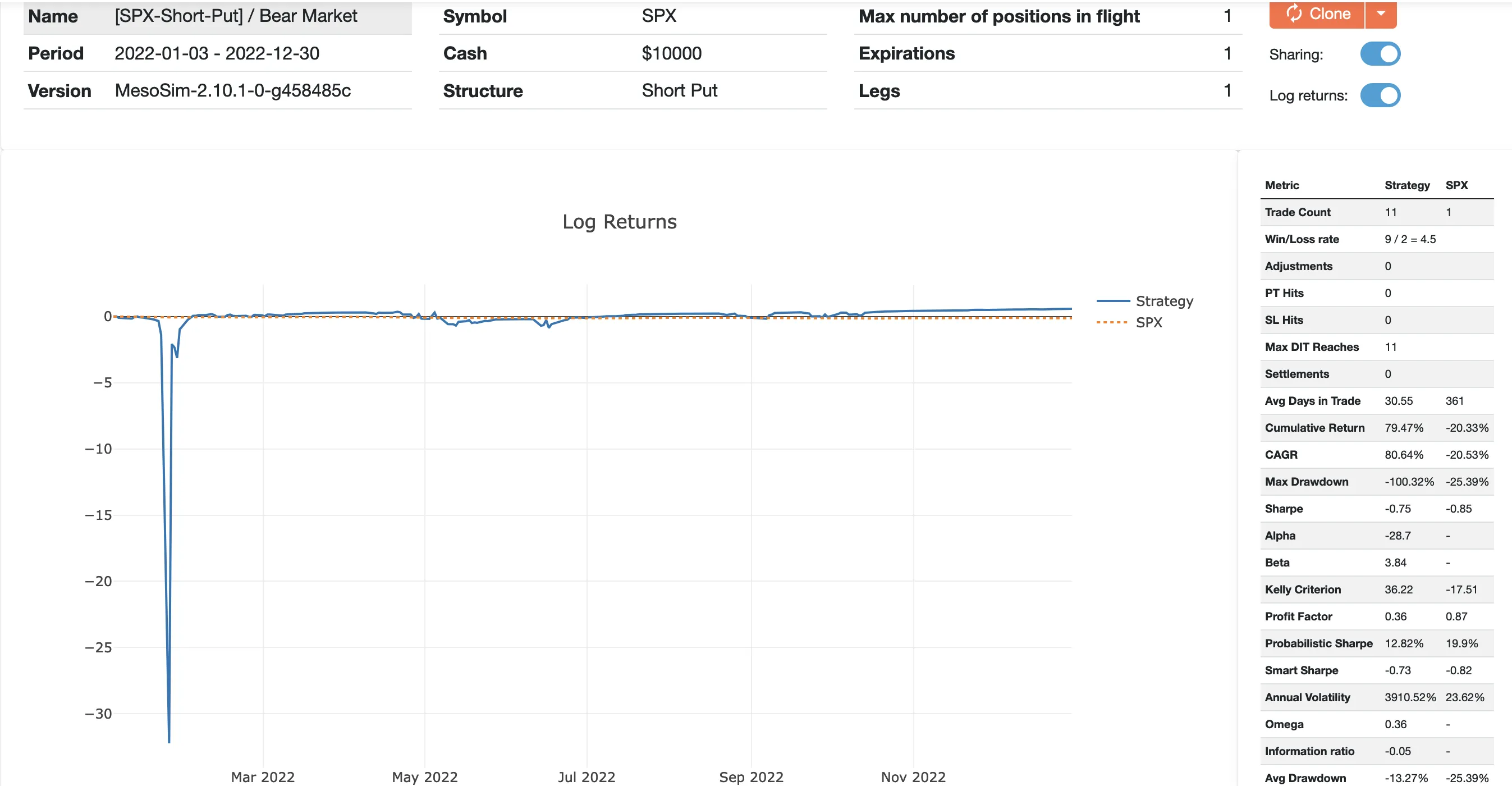

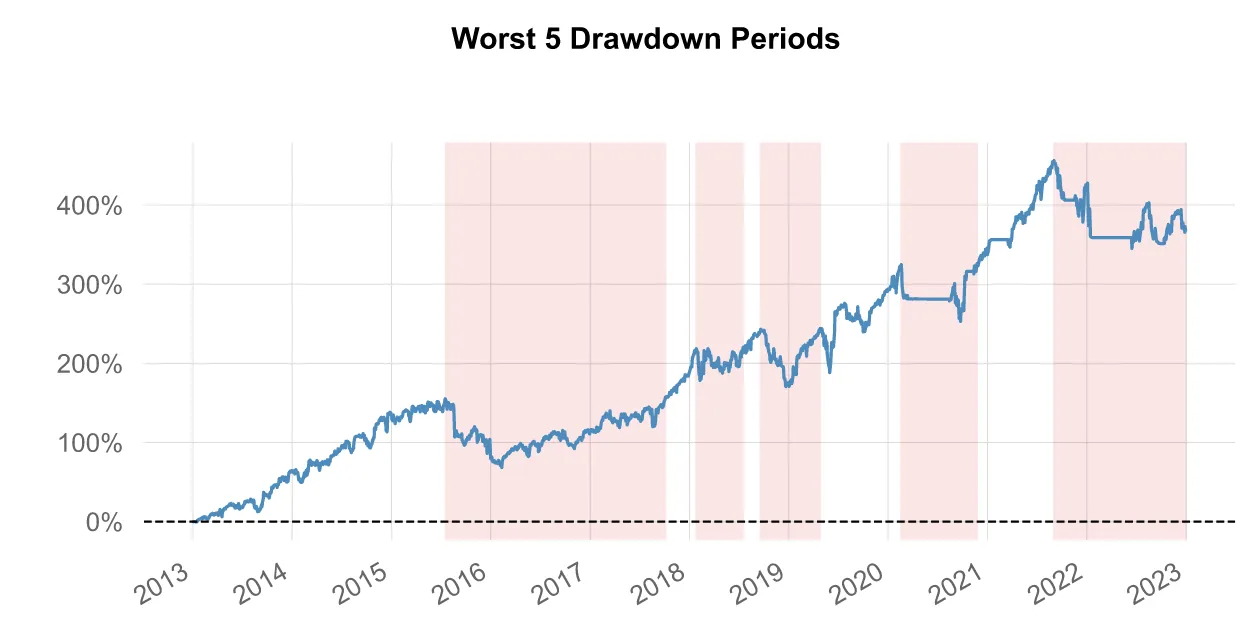

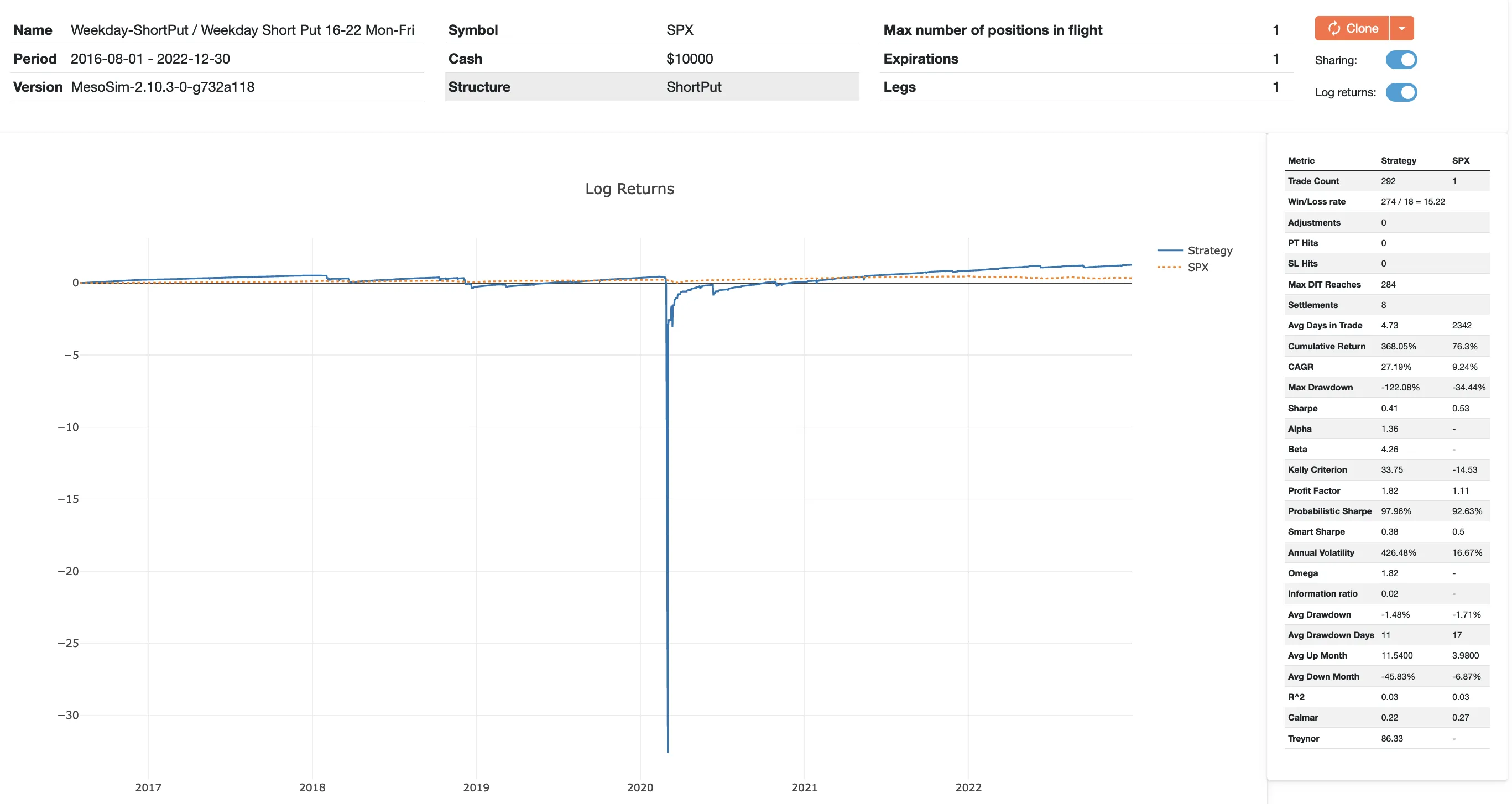

Short Put - Weekday version

To validate the existence of weekend premium, we modify the backtest’s entry and exit schedule to run to cover the opposite timeframe: Mondays to Fridays (4 DTE short put).

The strategy multiple times has drawdowns above 50%, including (but not limited to) the Covid crash period.

Backtest URL: https://mesosim.io/backtests/7f95f66e-f1be-4e8a-a524-d30f92229e71

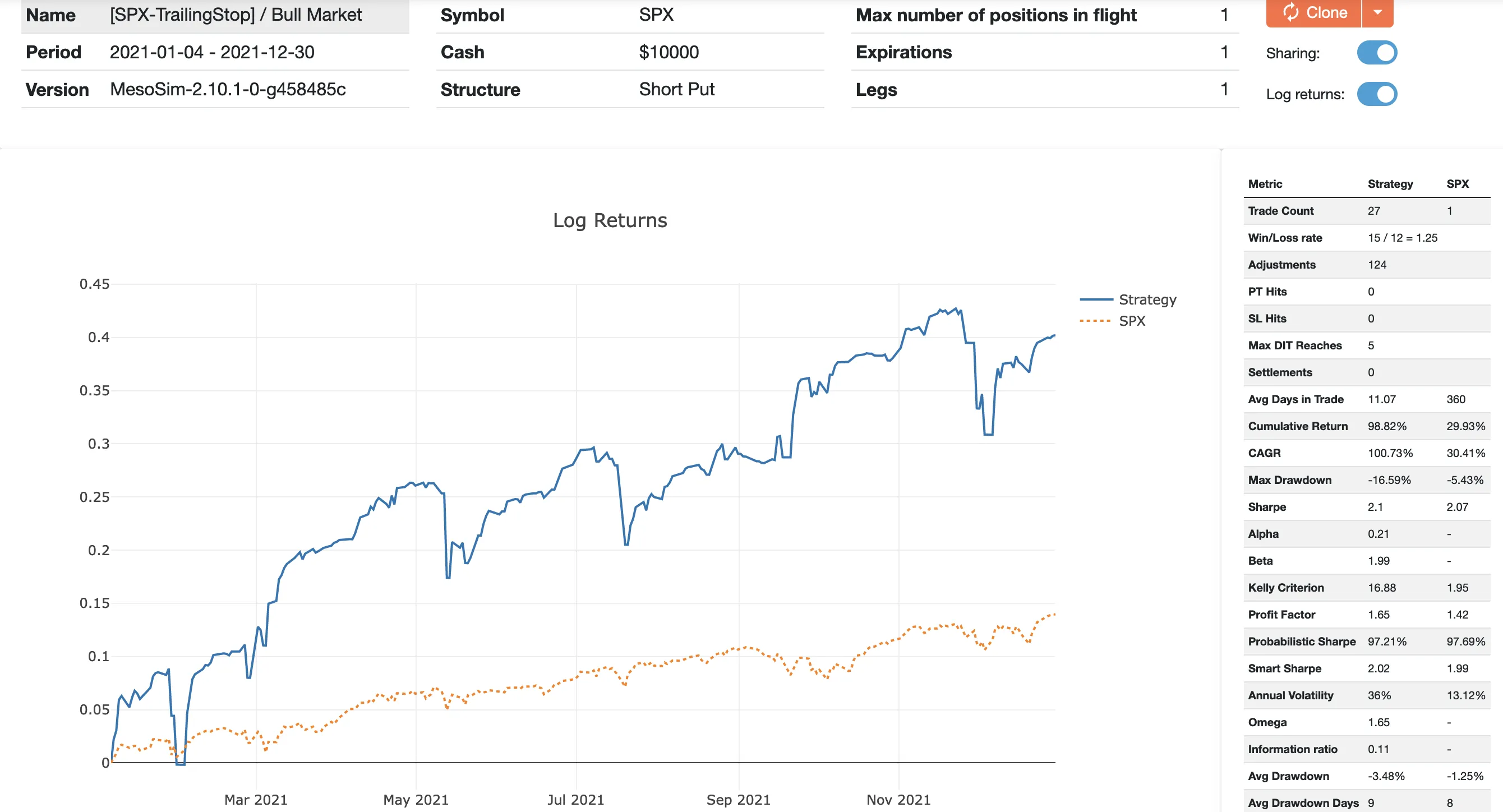

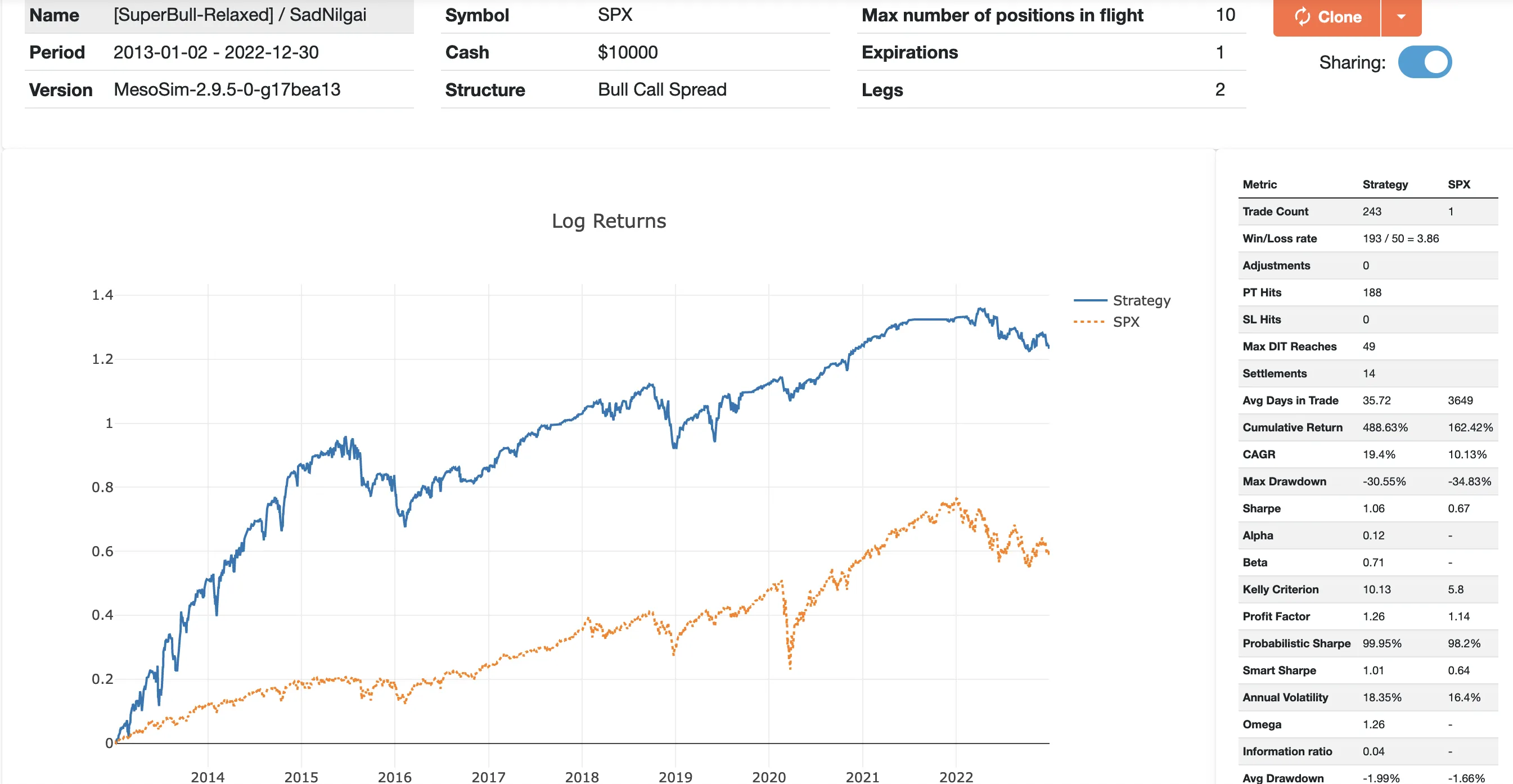

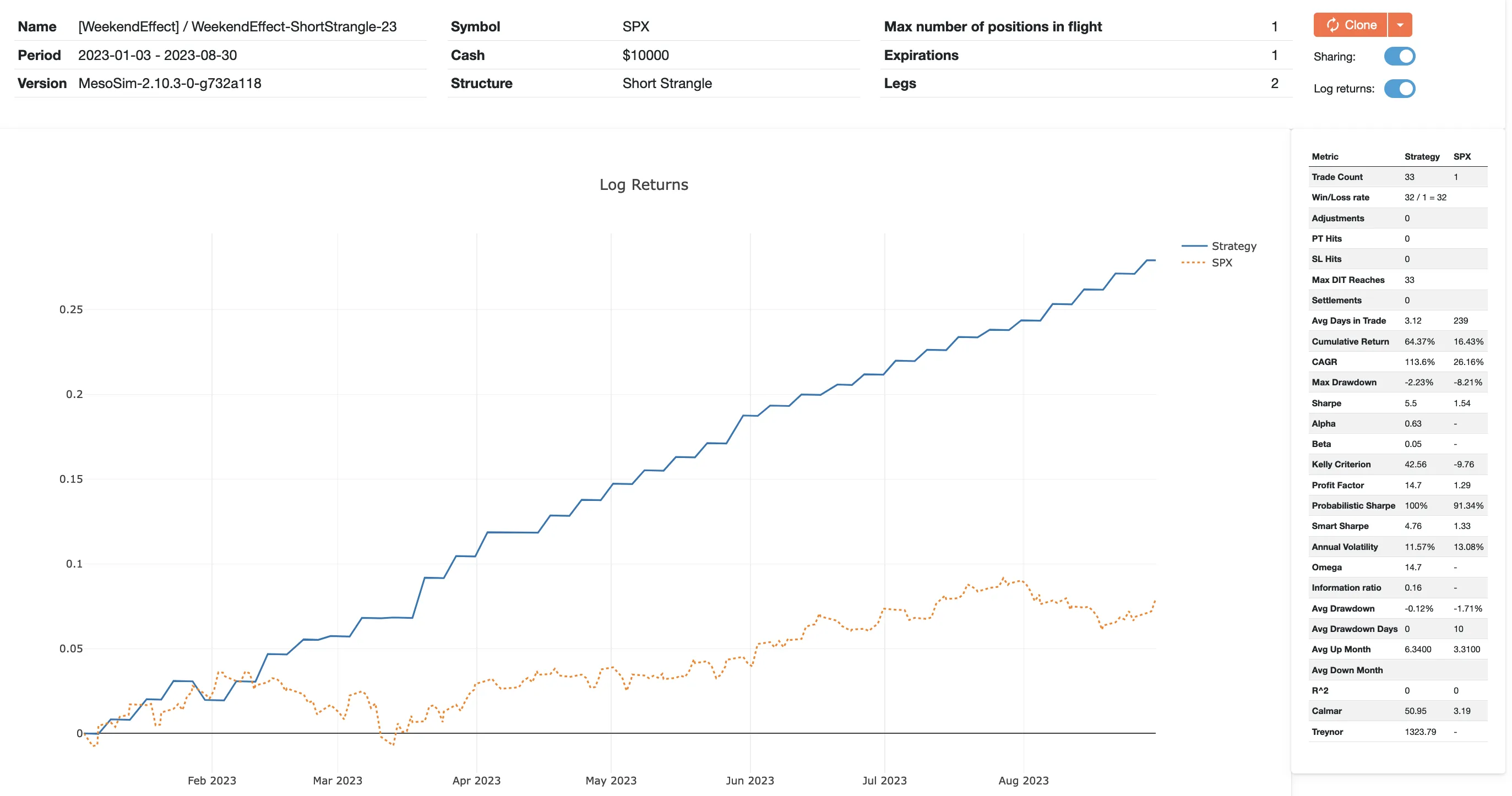

Short strangle

While the Short Put setup meets the Weekend Effect's instructions (sell options on Friday) and shows the effect in its purest form, it is possible to improve the strategy by selling more options:

If we sell Calls as well as Puts we end up having a Short Strangle structure. The collected premium is increased, therefore we expect larger returns. Since there is more risk on the downside, selling Calls likely won't increase our risk exposure.

Backtest URL: https://mesosim.io/backtests/e1b98b9c-cbb2-43f0-8abb-78ad1384e71f

- CAGR: 21.14% (Improved)

- Max Drawdown: -30.07% (Improved)

- Sharpe: 1.02 (slightly decreased due to higher volatility)

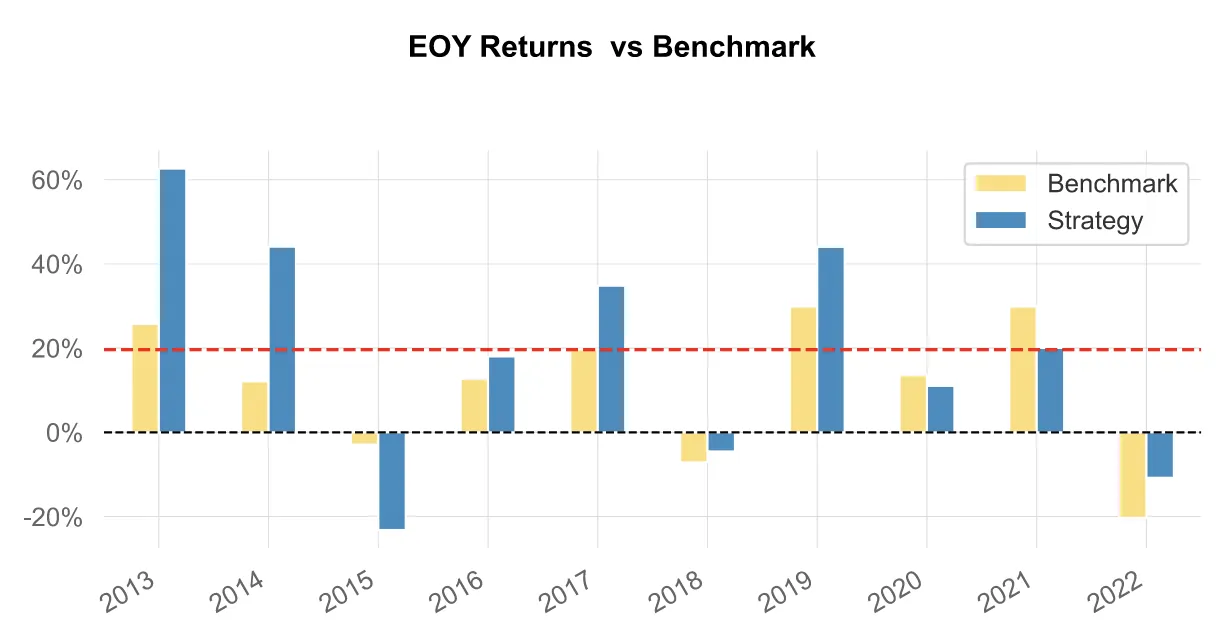

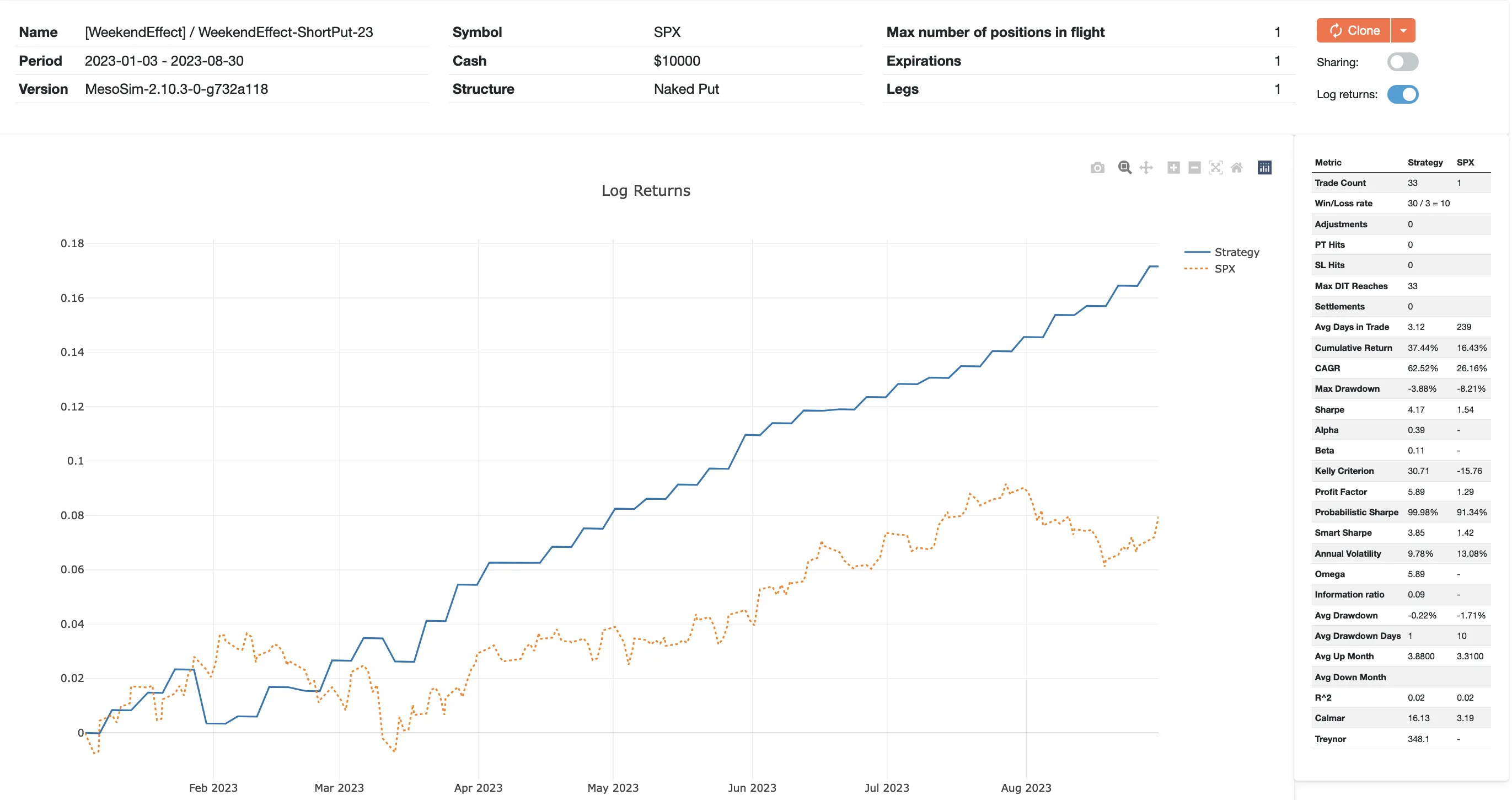

Backtest results: 2023

Finally, we run the Short Put and Short Strangle trades for the Weekend Effect in the most recent period: 2023. The results speak for themselves:

Conclusion and further work

Our analysis confirms the significance of the Weekend Effect when the strategy is backtested on S&P Index Options (SPX). Not surprisingly, the Strategy suffers its largest drawdowns during crash situations, such as COVID. Therefore, this (and any other option selling strategy) should be traded when adequate hedging is in place.

We would like to thank Euan Sinclair for spreading his knowledge via his excellent books and courses!

The Short Strangle version of the Weekend Effect is available in MesoSim as a built-in template, named: [WeekendEffect]

This article was originally written for MesoSim v2. The examples and terminology have been updated to match the MesoSim v3 Strategy Definition format. For details, see the MesoSim v3.0 release announcement and the v2→v3 migration guide. The performance metrics, described behavior, and referenced run results reflect the original v2 behavior. If you rerun the referenced strategies on MesoSim v3, results may differ slightly due to behavioral changes in the simulator.