Merlin v1.4 & Q-API v1.4 Release

Today we are releasing Merlin v1.4 and Q-API v1.4, introducing significant enhancements in our machine-learning-based strategy-optimization toolkit.

These additions address recurring challenges in options-trading research: non-linear relationships, feature redundancy, and scale differences—that can degrade model performance.

These updates are exclusive to Deltaray FundPro subscribers.

Improvements

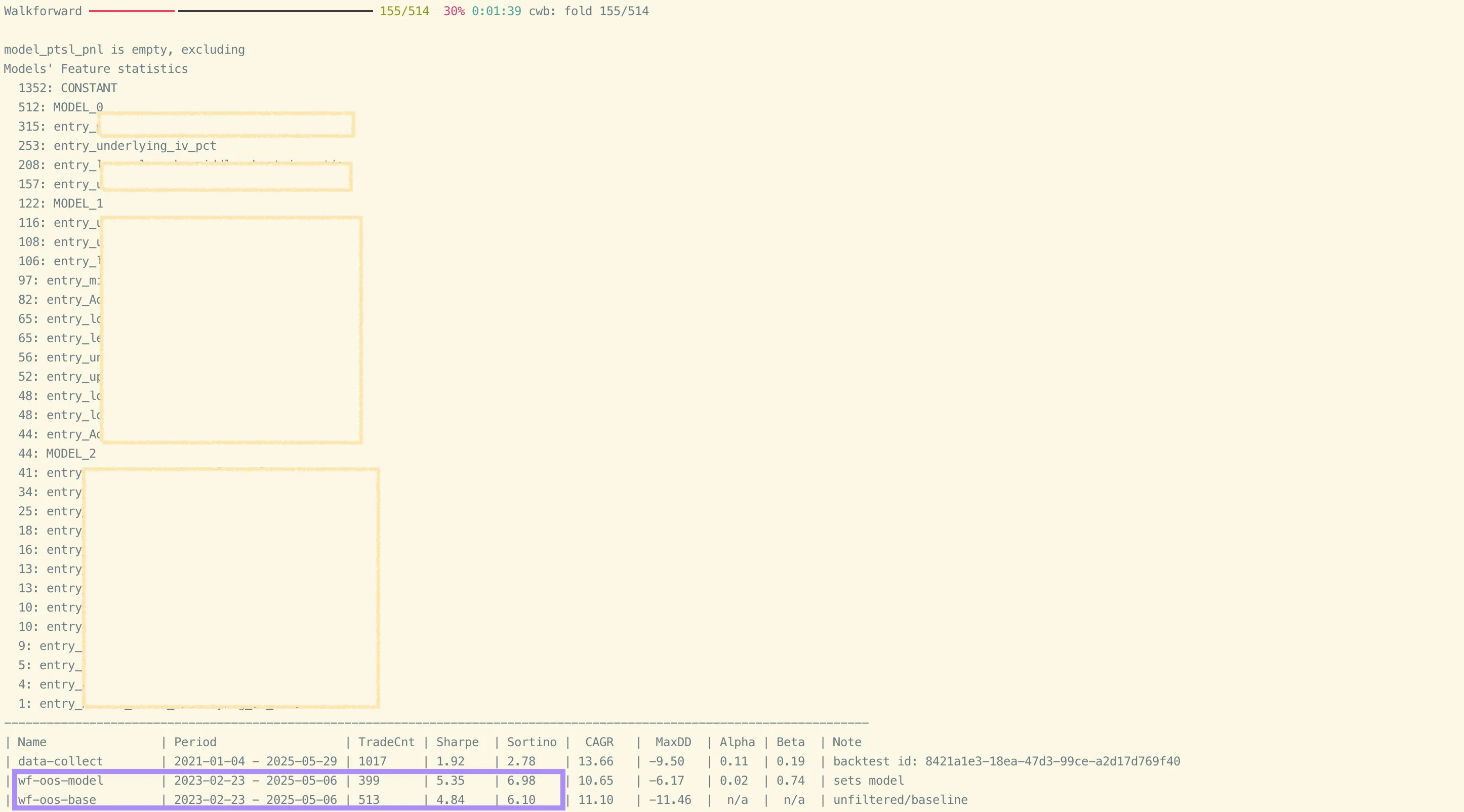

SETS Model: Logistic & Quadratic Regression

The Stepwise Ensemble for Trade Selection (SETS) model is a specialized predictive-modeling approach designed for systematic strategy development. It automatically discovers patterns in historical results and builds an optimized ensemble of regression models to forecast future market behaviour.

The models built with SETS can serve as trade filters and position-sizing optimizers in strategies created with MesoSim.

New in Q-API v1.4: logistic and quadratic regression are now supported alongside linear models, expanding the toolkit for datasets with different target types and shapes.

Logistic Regression

Logistic regression maps a linear predictor to a probability via the logistic function:

P(y=1) = 1 / (1 + e^(-(β₀ + β₁x₁ + ... + βₙxₙ)))

Useful when

- the target distribution contains extreme outliers that would skew linear-regression coefficients, or

- classification accuracy (win/loss) matters more than point estimates.

Logistic, quadratic, and linear specifications can be freely mixed inside one SETS ensemble.

Quadratic Regression

Quadratic regression augments the linear model with squared and interaction terms:

y = β₀ + β₁x₁ + β₂x₂ + β₃x₁² + β₄x₂² + β₅x₁x₂ + ε

This captures curvature without the complexity of higher-order polynomials or deep networks.

In our implementation, polynomial expansion occurs during preprocessing to optimize inference performance.

MIFS: Mutual-Information-Based Feature Selection

Q-API v1.4 comes with a new model: MIFS—Mutual Information based Feature Selection.

Feature redundancy is a frequent cause of overfitting; MIFS leverages information-theory metrics to retain only the variables that add unique predictive power.

Key components:

| Step | Purpose |

|---|---|

| Mutual Information (MI) | Quantifies how much knowing a feature reduces uncertainty in the target. MI is estimated with binned entropy estimators. |

| Monte-Carlo Permutation Test | Evaluates whether an observed MI score is significant or could arise by chance. |

| Chi-square & Cramér’s V | Provide an effect-size measure for categorical associations, extending beyond linear correlation. |

MIFS acts as a pre-screening step before SETS model training: Statistically validated, non-redundant features fed into SETS improve generalization while shortening training times.

Feature Transforms in Merlin

Merlin, our strategy- and portfolio-optimizer, now offers full-support for feature-transformation modes.

During feature engineering phase, the raw features are transformed to add memory and induce stationarity using standardization techniques.

The transformed features are now can be synthesized into MesoSim backtests and used in live trading with MesoLive.

Results

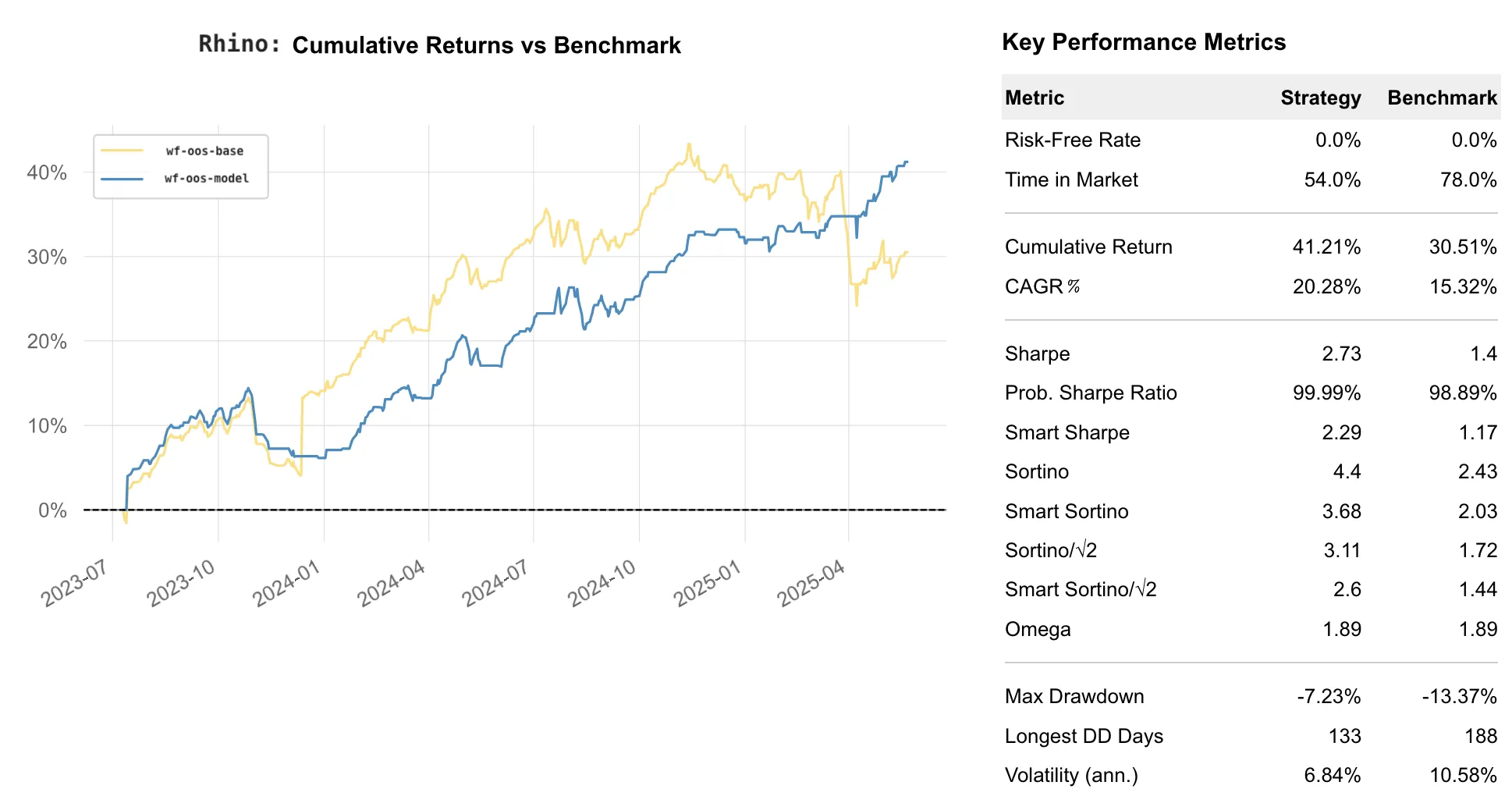

Across calendars, iron condors, broken-wing butterflies, iron flies, bwb+cal combos at various maturities the optimizer managed to increase Sharpe ratios with an average of 0.52 while reducing the time in market by 22% across 12 trading strategies.

The strategies are employ a wide variety of holding times, maturities and moneyness.

Next Steps

Our results confirm that, with the right tooling, tradable alpha can be extracted from the option chain.

While Merlin currently derives signals from the actively traded structure, the next milestone is to capture alpha using the full volatility surface.

In parallel, the MesoLive infrastructure is being upgraded to support additional brokerages, delivering broader venue choice and greater resilience for live strategies.