Skew This: NetZero

Intro

The last 12 to 18 months have been challenging for (the well-known) options strategies using medium- to long-dated tenors. A prolonged period of stagnation was followed by a crash (VolZilla), which unfortunately led to higher-than-usual drawdowns or, in some cases, completely wiped out accounts. Some attribute these results to skew dynamics, while others associate it with the end of the Zero Interest Rate Policy (ZIRP).

Skew in Options Market

"The volatility skew is the difference in implied volatility (IV) between out of the money options (OTM), at the money options (ATM) and in the money options (ITM). The volatility skew, which is affected by sentiment and the supply and demand relationship of particular options in the market, provides information on whether traders and investors prefer to write calls or puts."

Source: Investopedia

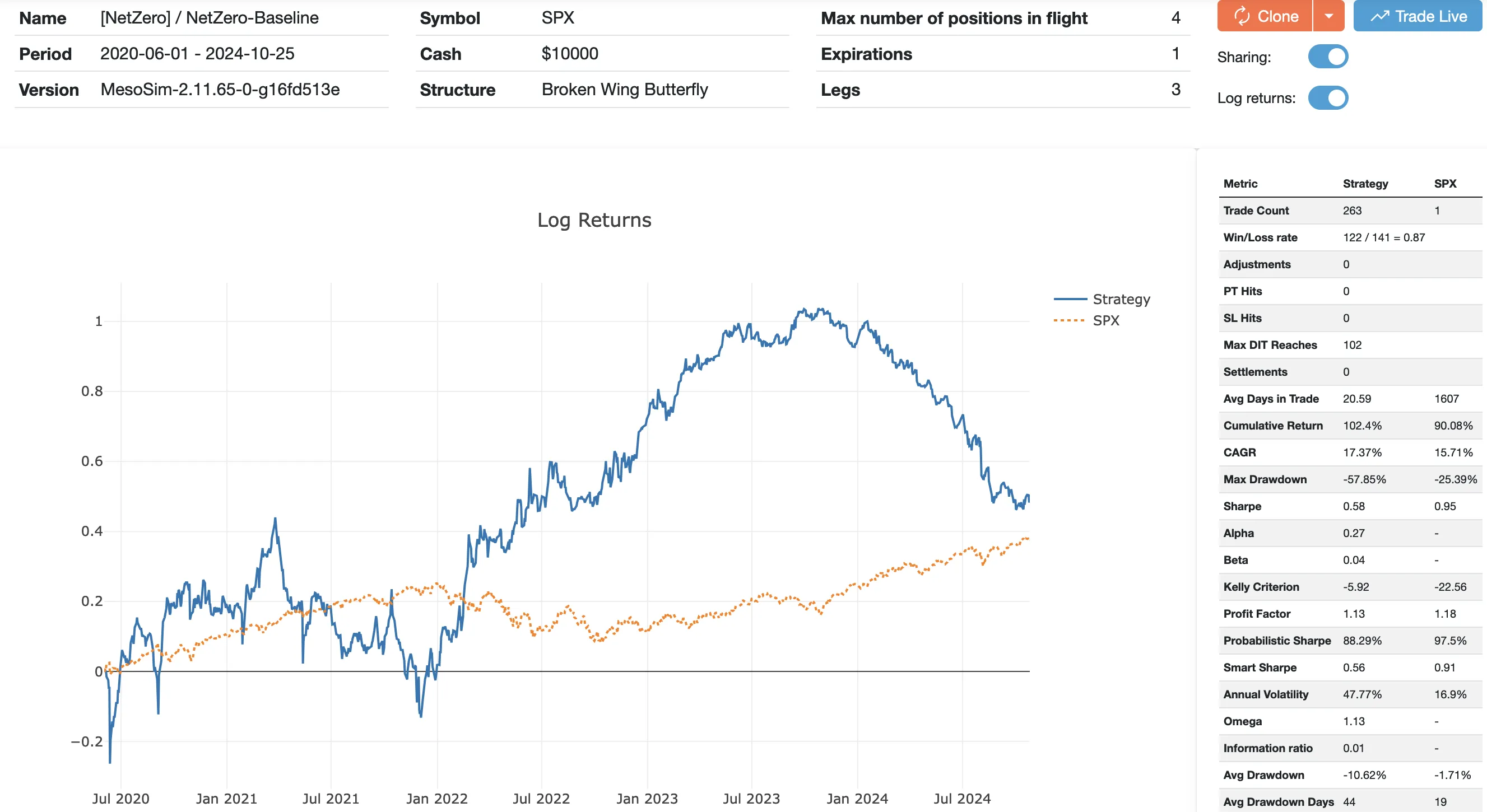

NetZero performance

The NetZero trade also suffered during this period.

After a half-year of stagnation, it began to consistently lose money in 2024.

Run: https://mesosim.io/backtests/86ab8fb0-92d6-4e5b-99e8-4e9c52d4ab67

Grid Search results

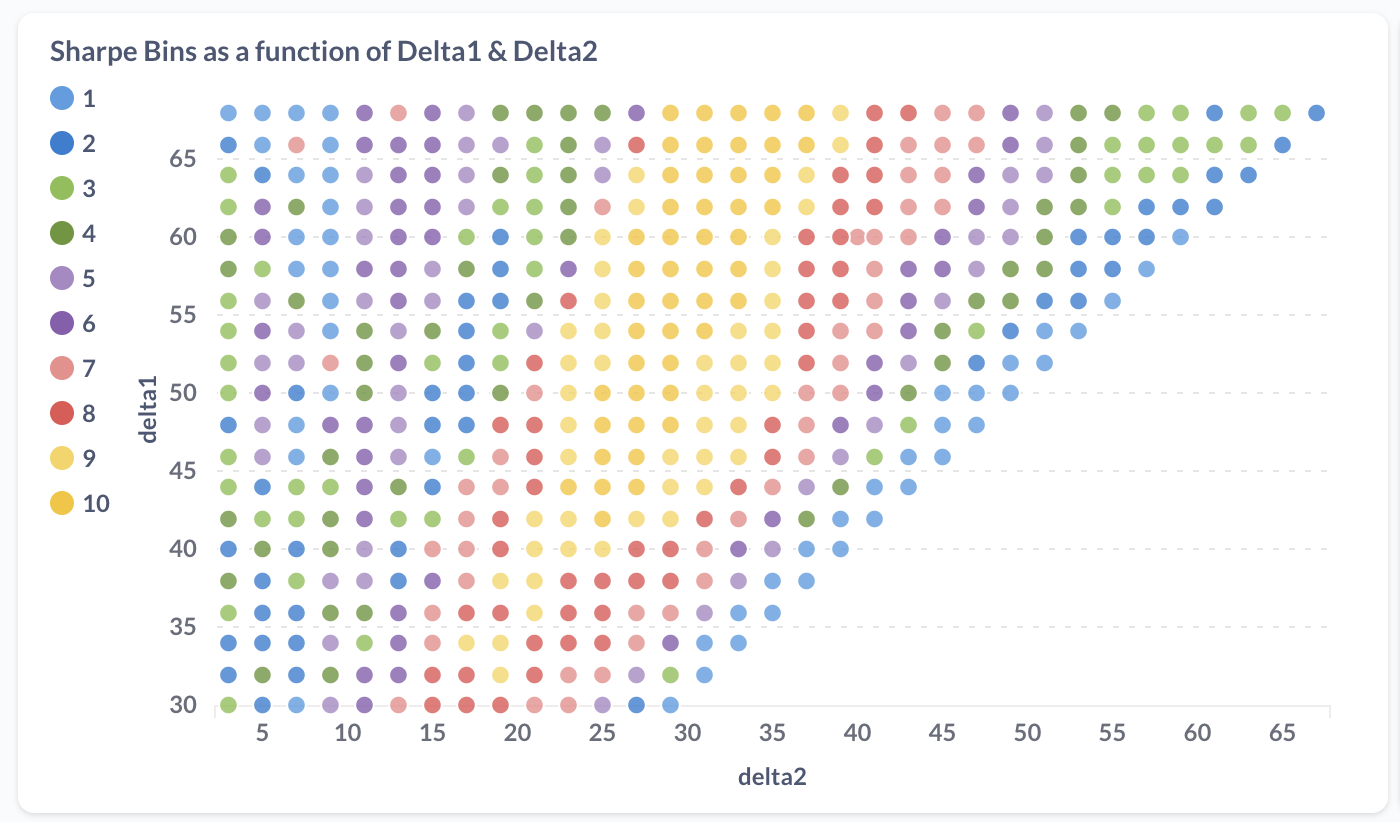

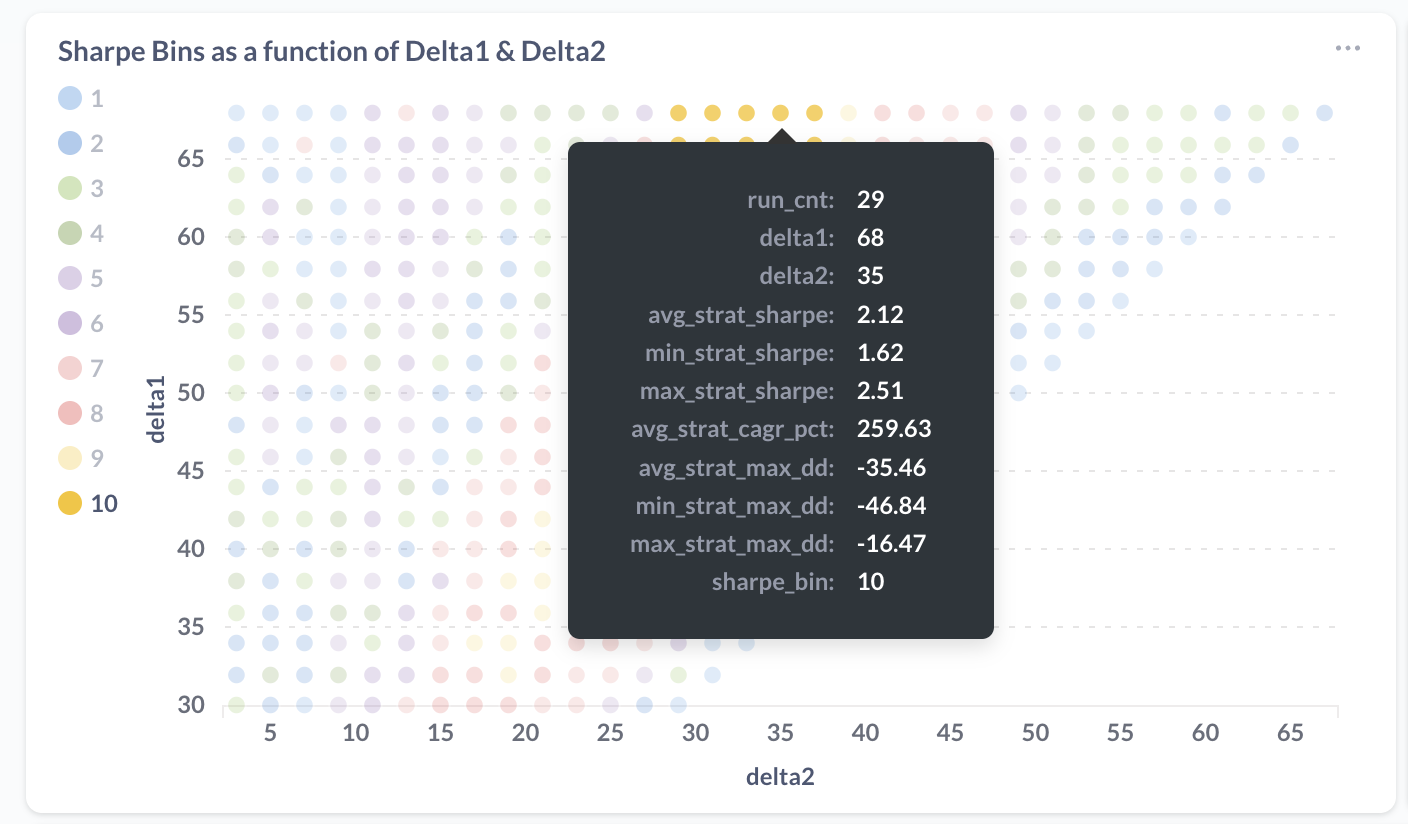

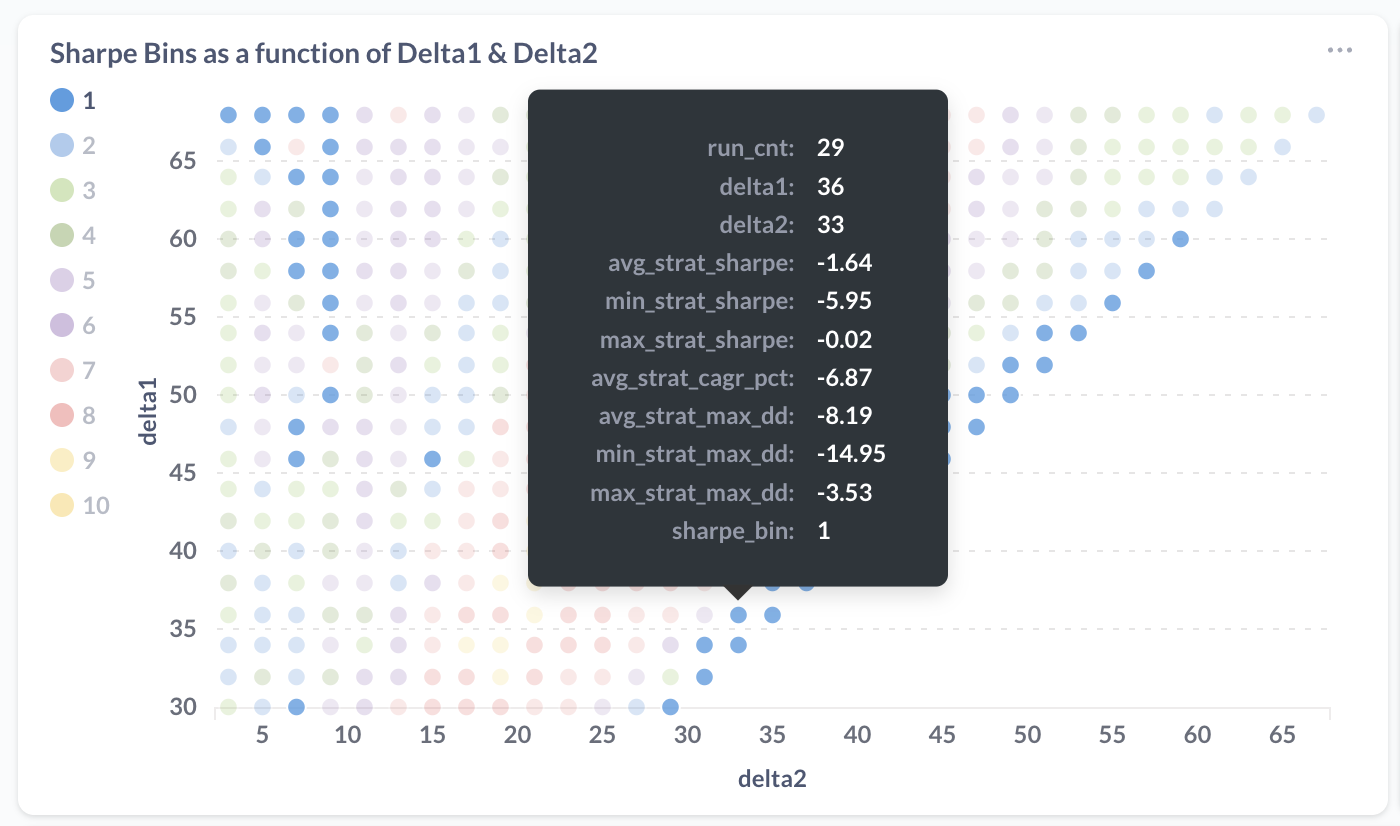

To have a more complete picture of the trade performance in 2023 we ran a Grid Search, iterating over various DTEs and leg deltas while retaining the original trade rules and targeting a delta-neutral setup. Our experiment includes 13,633 unique runs.

To visualize the results, we summarize them by displaying the average Sharpe ratio for different delta combinations, as well as the average Sharpe ratio calculated across various DTEs from 5 to 70 (including all delta combinations).

Effect of skew changes

From the above runs it is apparent that the trade performs best when the short positions are set closer to 30 deltas, while the upper long positions are near 70 deltas. The original trade plan placed these legs at 40 and 60 deltas, respectively. The results also suggest that there is now a relatively narrow profitable range for this trade.

Out of Sample validation

The best In-Sample result for the 2023 experiment provides a significant improvement over the original 2023 result:

NetZero 2023 OriginalBest in-sample run:

https://mesosim.io/backtests/b99c17bb-ad34-4535-93b3-35203e03335f

Original run:

https://mesosim.io/backtests/51714548-7374-4f4f-a686-6169fc4b6339

When we take the best in-sample result and apply it to 2024, it does improve performance compared to the original trade plan but does not make the trade significantly successful in the out-of-sample period.

2024NetZero-opt-OOS-2024:

https://mesosim.io/backtests/347a2654-e628-42b7-9344-3aaef4548790

NetZero-original-2024:

https://mesosim.io/backtests/211c3990-73bf-4f4c-ab3a-23ef0db79c24

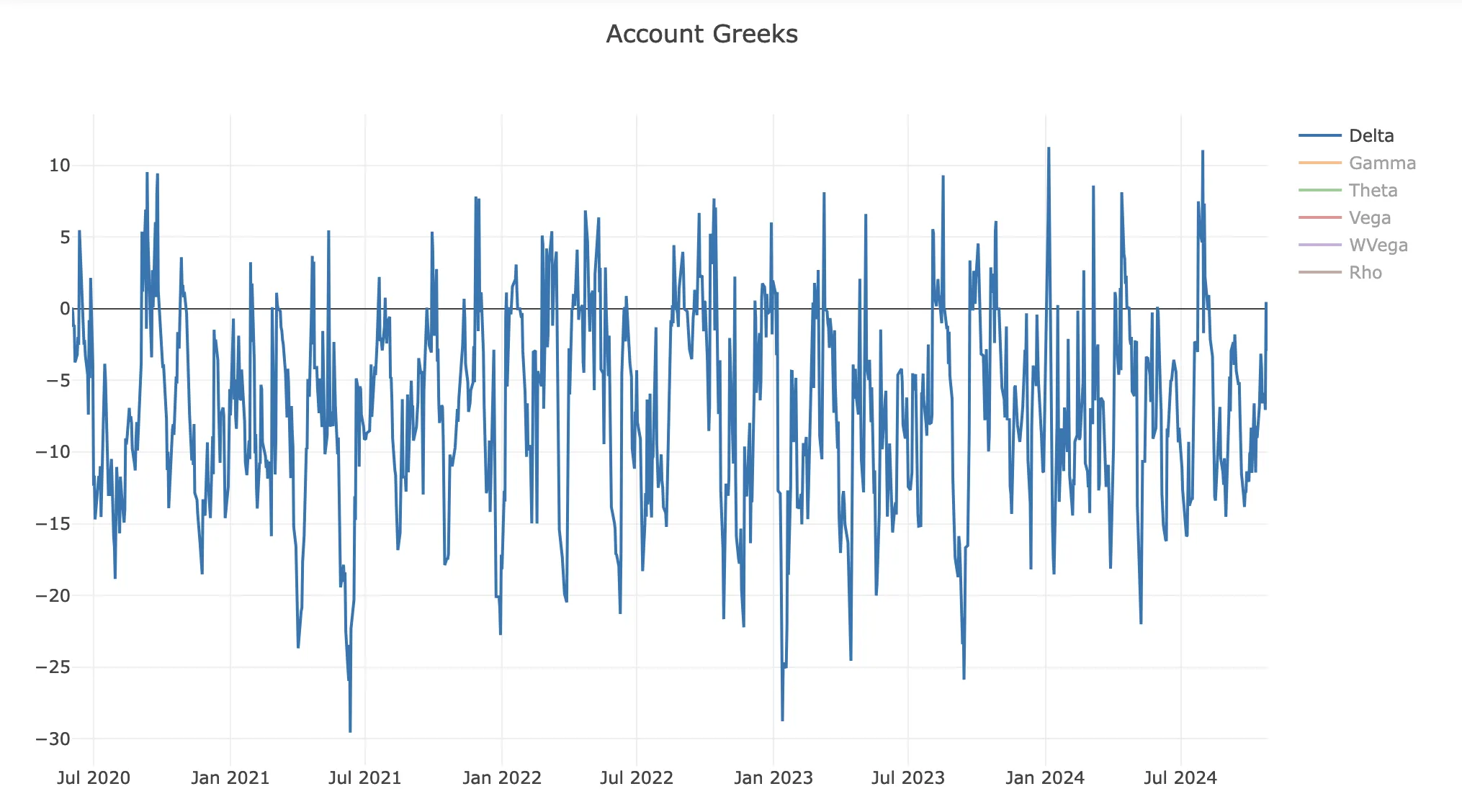

Keeping it delta neutral

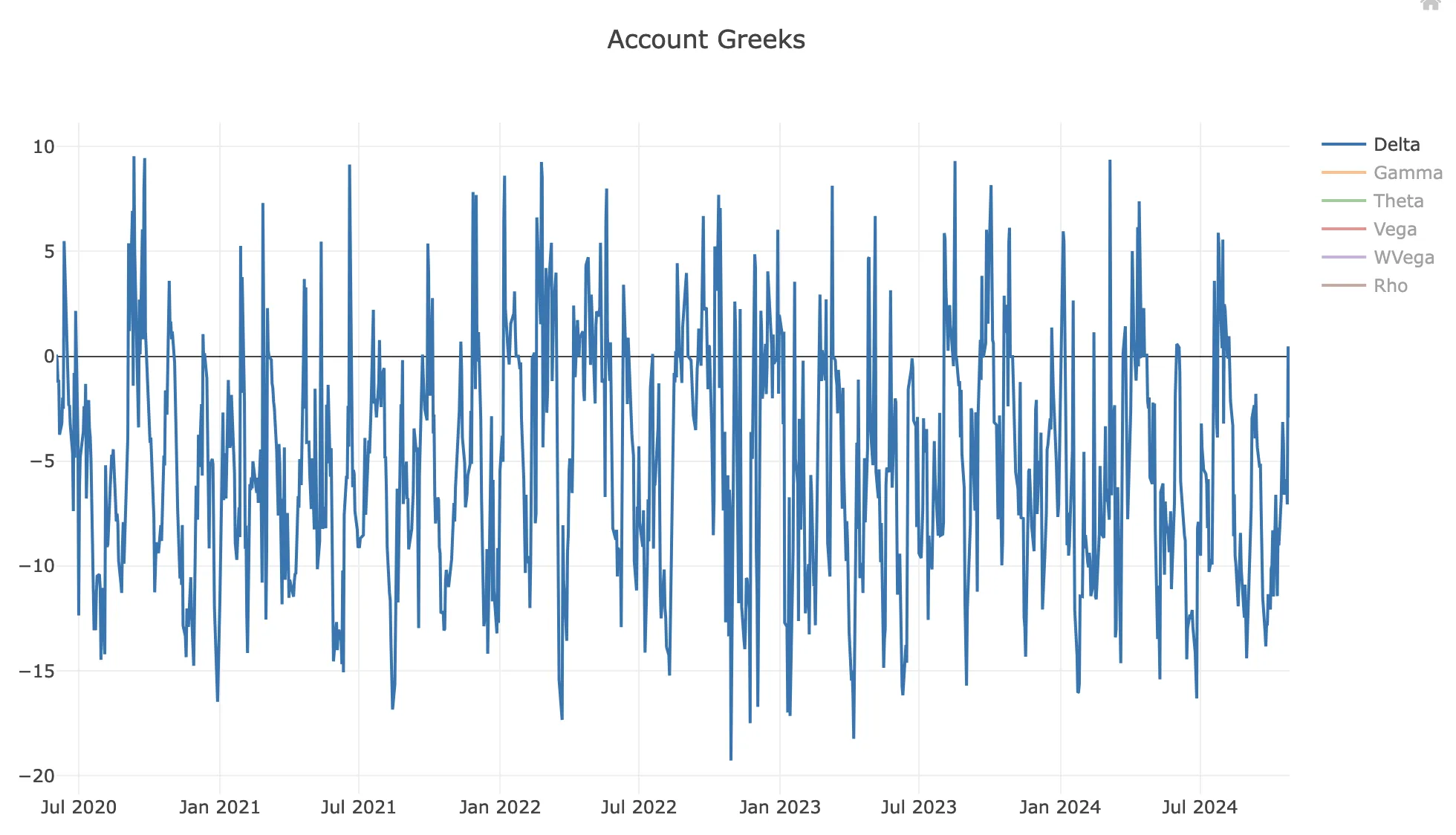

Studying the account (strategy) Greeks reveals that the original trade spends most of its time in negative delta territory, which is not advantageous in a bull market like the one in 2024. Although our NetZero variant included an exit condition (exit when the trade becomes too directional: abs(delta) > 10), we conducted an experiment here to adjust one of the legs rather than resetting the entire structure with tighter thresholds.

This can be achieved using MesoSim’s ConditionalAdjustment feature:

Whenever the Position Deltas are reaching a certain threshold, we move one of the legs to keep the structure delta neutral:

"ConditionalAdjustments": {

"abs(pos_delta) > 5": {

"MoveLegAdjustment": {

"LegName": "upper_long",

"StrikeSelector": {

"Delta": "abs(leg_upper_long_delta - pos_delta) / abs(leg_upper_long_qty)"

}

}

}

},

Since the strike selector for the MoveLeg adjustment is evaluated while the original structure is still active, we need to account for the removal of the existing leg and the addition of a new one. This leads to the formula specified in the Delta Strike Selector. You can read more about delta hedging concepts in MesoSim here.

While the trade directionality reduced, the end result is still similar to our baseline run:

Full-period:

https://mesosim.io/backtests/1b8bc34c-521a-4117-bcc1-498a4a731a90

2024:

https://mesosim.io/backtests/77760921-731c-4355-aedc-1ce310e74dd2

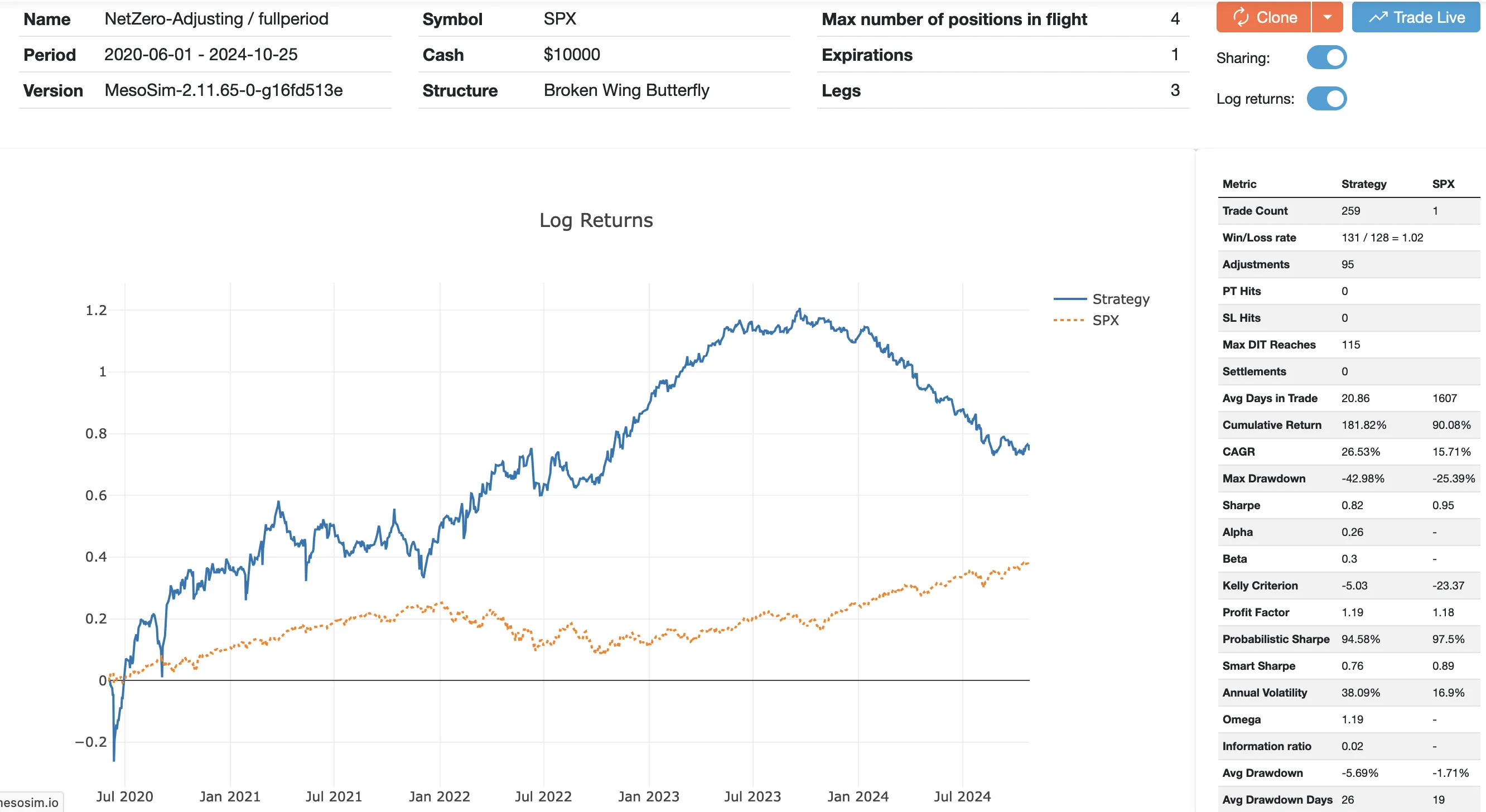

Inverting the structure

The sharp and consistent decline in strategy pnl in 2024 made us wonder:

How would it perform if we turn it upside down?

While it may seem reasonable to expect a positive outcome from this experiment, this approach typically does not work for broken strategies. Strategies that trade excessively on weak signals (noise trading) usually cannot be salvaged in this way.

In the NetZero case, this would mean transforming the Broken Wing Butterfly structure into an Inverted Broken Wing Butterfly. This can be easily achieved by setting the Entry.QtyMultiplier=-1 .

The original vs resulting structure:

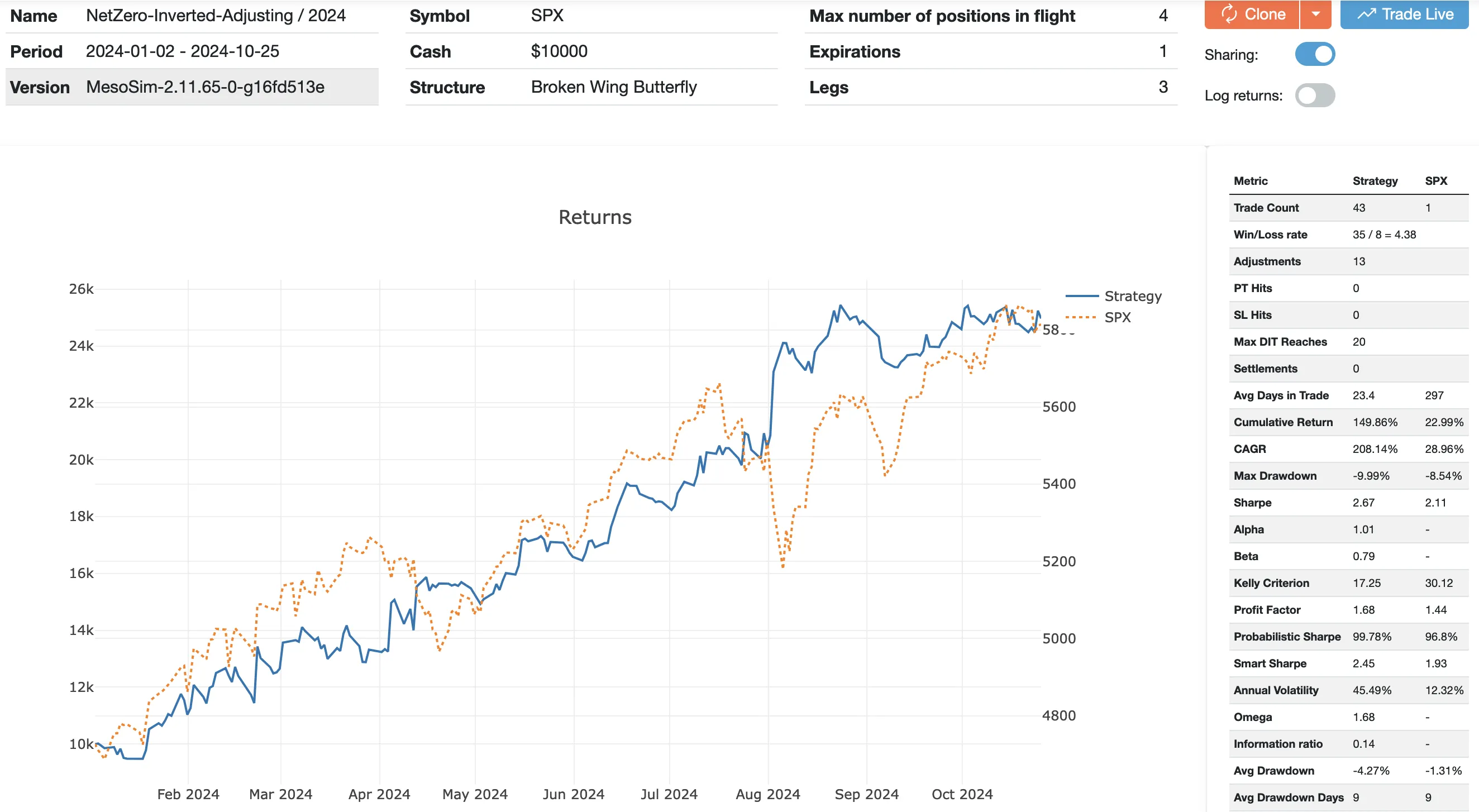

The results for the full period aren’t particularly appealing, but for 2024, they are greatly improved: the previously losing strategy became profitable.

NetZero-Inverted-2024:

https://mesosim.io/backtests/3517be29-ef50-4548-95f0-3bbd8baddfa1

NetZero-Inverted-fullperiod:

https://mesosim.io/backtests/92ab5815-a79b-45e2-a469-270120e3d634

We do not suggest that trading this strategy in an inverted manner is a reasonable approach.

Instead, it serves as another way to represent the current market profile.

Conclusion

In this article we took a public trade and studied it’s relation to the skew by running a Grid Search with various deltas for the long and short legs. We found that the now-optimal trade setup has drifted quite a bit from the original trade plan. Optimizing the deltas using the 2023 period and validating in 2024 yields better results than the original, though still not particularly appealing.

However, inverting the trade structure significantly boosts its performance for 2024.