MesoSim v2.4: Relative Expiry, Risk Graph and new templates

We are happy to report that a new release of MesoSim is landed, which extends the functionality of Expirations, pre- and post-trade Analysis with Risk Graphs and Full TearSheet and provides a handful of new Templates to get you started more quickly.

Expirations:

We incorporated your feedback and implemented Root / OCC Symbol Selector and Relative Expirations. In practice, you can now filter (for example) for Weekly SPX Options and elegantly define calendar spreads by specifying the second expiration based on the expiration chosen for the first.

Please see the Structure section of the Documentation for further details.

As a sample, we created the Enter-RootSelector and Calendar templates, which are available in the portal.

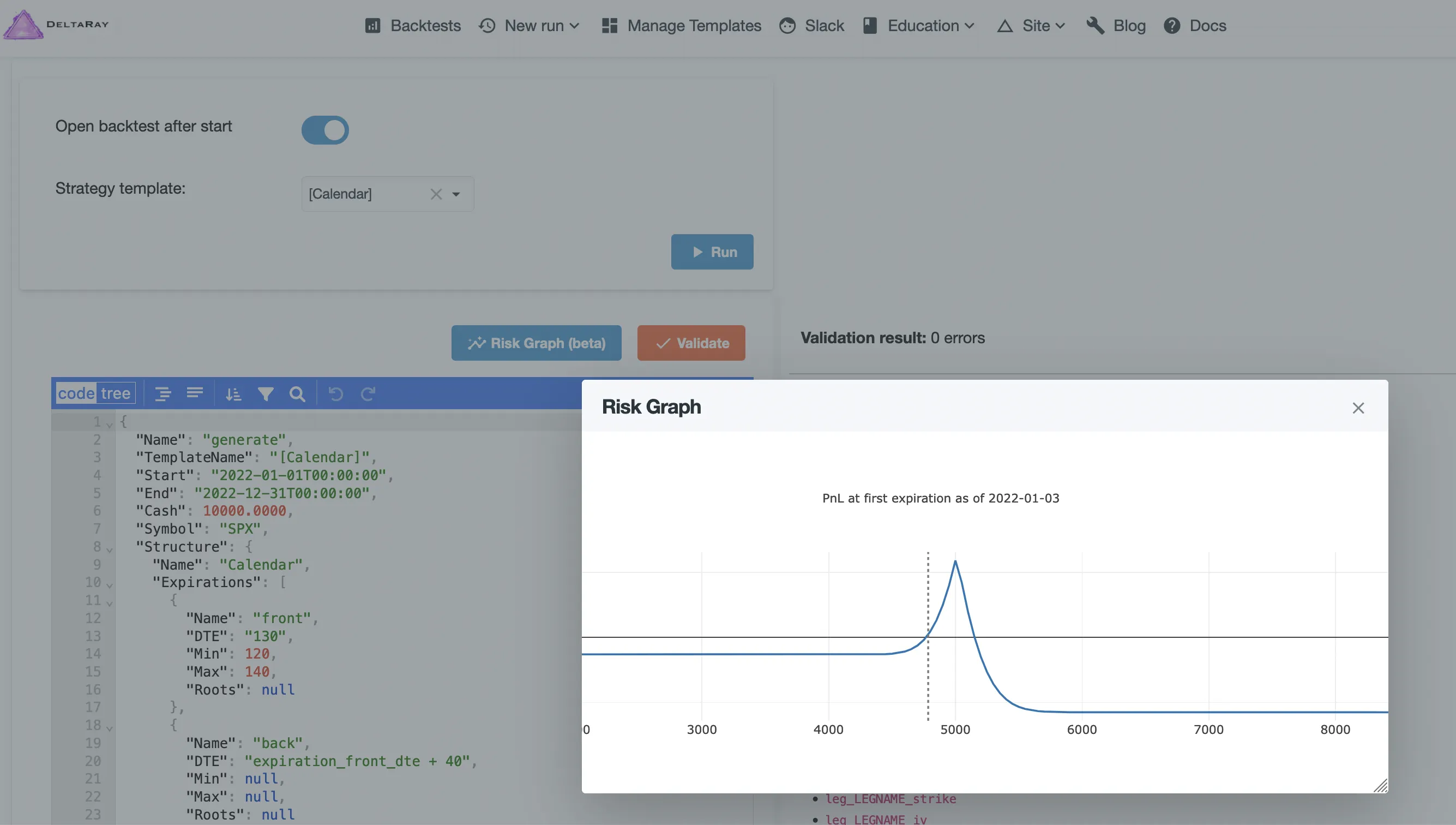

Risk Graph in JobEditor

We added the initial version of Risk Graph to JobEditor, so you can now see what you are building (without importing it to ONE). The Risk Graph is calculated and shown based on the first entry your backtest would make.

Please note that this isn't the final version, additional features, such as T+x lines and greeks are coming shortly!

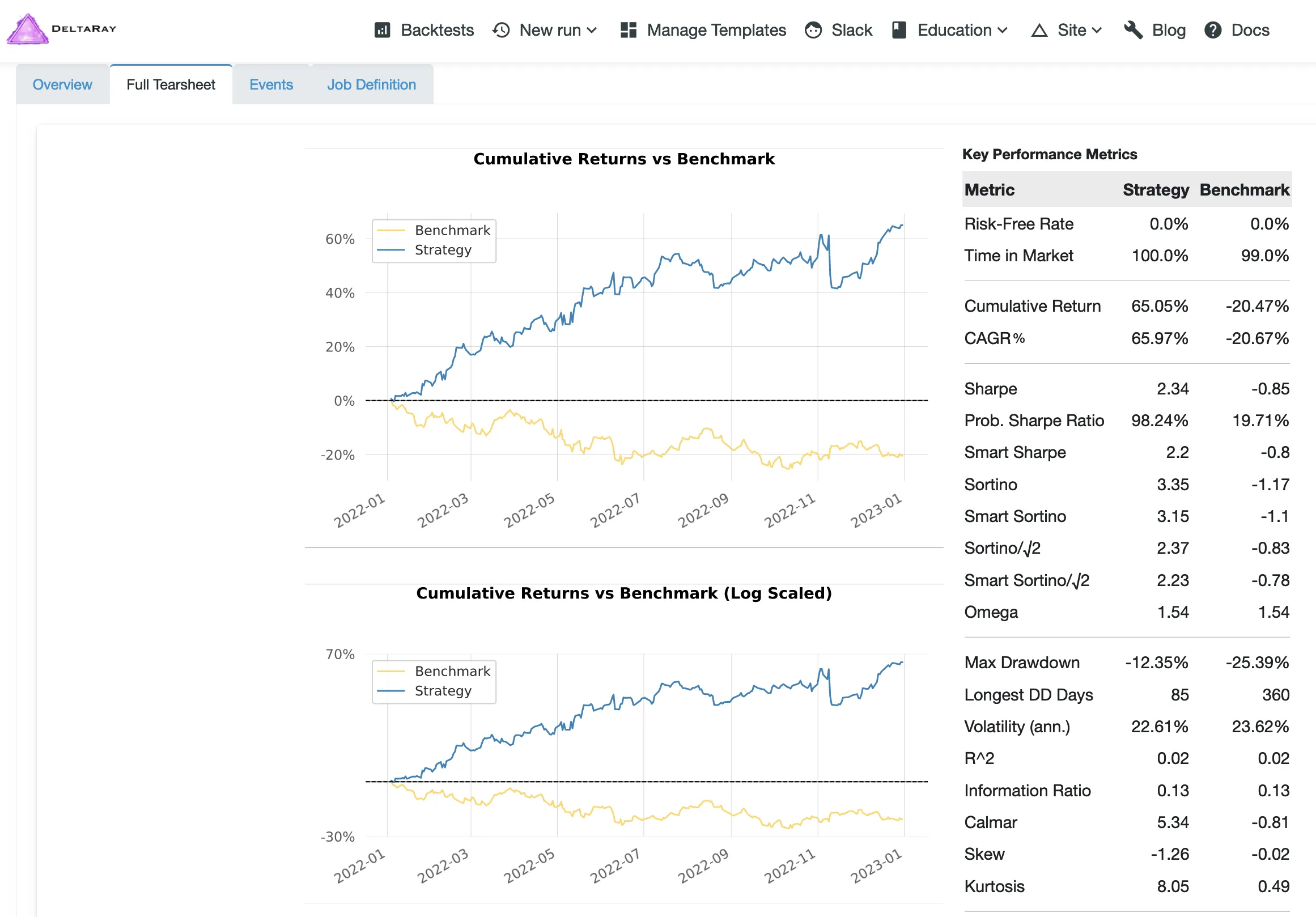

Full TearSheet

We have extended analytic capabilities by including Ran Aroussi's excellent QuantStats package. You can access it by clicking the 'Full Tearsheet' tab on the backtest details page.

New Templates

We did a bit of housekeeping in the existing templates and categorized them better based on their functionality.

Examples of basic Options structures are included:

While filters are listed under their respective sections:

Finally, we added a set of ready-to use strategies:

the old-school NetZero trade did pretty good in 2022.

We hope you enjoy this new release!

This article was originally written for MesoSim v2. The examples and terminology have been updated to match the MesoSim v3 Strategy Definition format. For details, see the MesoSim v3.0 release announcement and the v2→v3 migration guide. The performance metrics, described behavior, and referenced run results reflect the original v2 behavior. If you rerun the referenced strategies on MesoSim v3, results may differ slightly due to behavioral changes in the simulator.